Fund Selection — July 2025

Panel

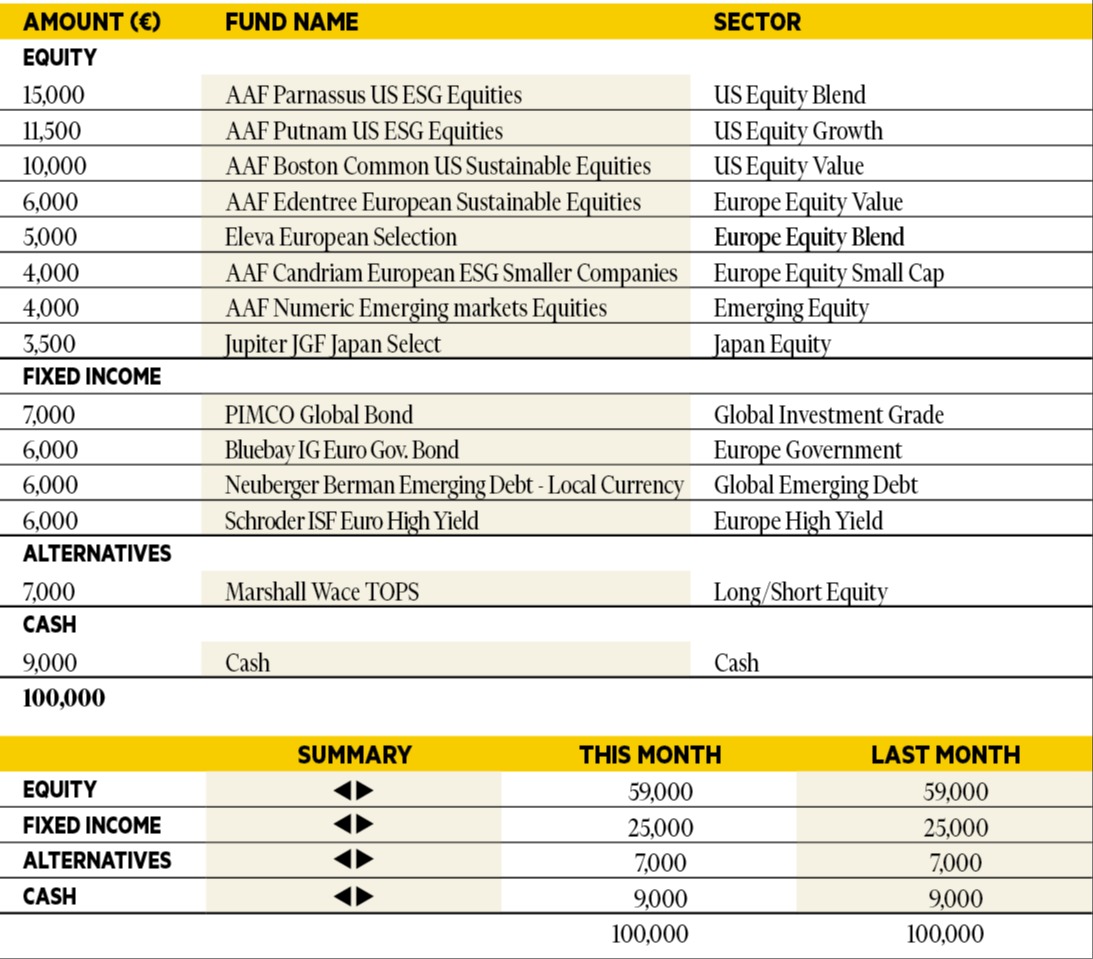

Benjamin Hamidi

Senior portfolio manager, ABN AMRO Investment Solutions.

Based in: Paris, France

“The labour market and the economy remain robust. US fiscal policy would be accommodative, with a larger deficit forecast, which should support activity, but could make the debt trajectory less and less sustainable. The market is therefore lowering its expectations for Fed rate cuts over the coming months. The end of the tariff suspension period is near, but the market is convinced at this stage that agreements will be signed or that the suspension will be extended. Against this backdrop, we are maintaining a moderate diversified asset allocation, and we are keeping a close eye on the ongoing negotiations.”

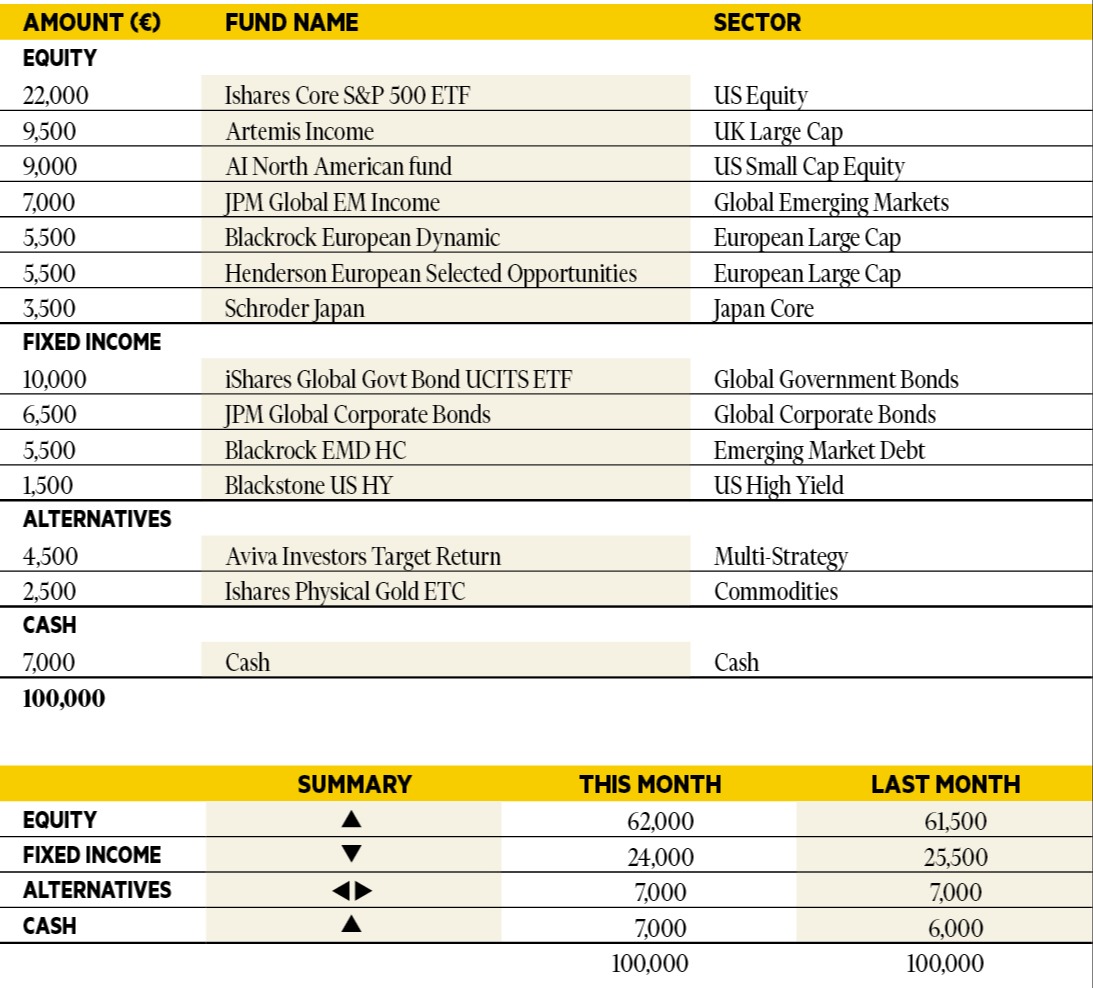

Luca Dal Mas

Senior fund analyst, Aviva Investors.

Based in: London, UK

“In June, we experienced US strikes on Iranian nuclear facilities, but a quick ceasefire and muted Iranian retaliation lead to a sharp drop in oil prices. After a volatile start, equity markets reacted well and moved higher during the period. In Europe, Germany unveiled a front-loaded fiscal stimulus plan, boosting sentiment and lifting domestic indicators. General Eurozone data was mixed, with Germany improving but peripheral economies and France showing signs of weakness. In the US, economic data softened, with Q1 GDP revised down, while inflation risks persisted due to rising input prices and tariff effects. Central banks, including the ECB, are expected to continue easing, with rate cuts priced in for late 2025. In portfolios we have marginally increased our exposure to US equities while trimming our local bond allocation.”

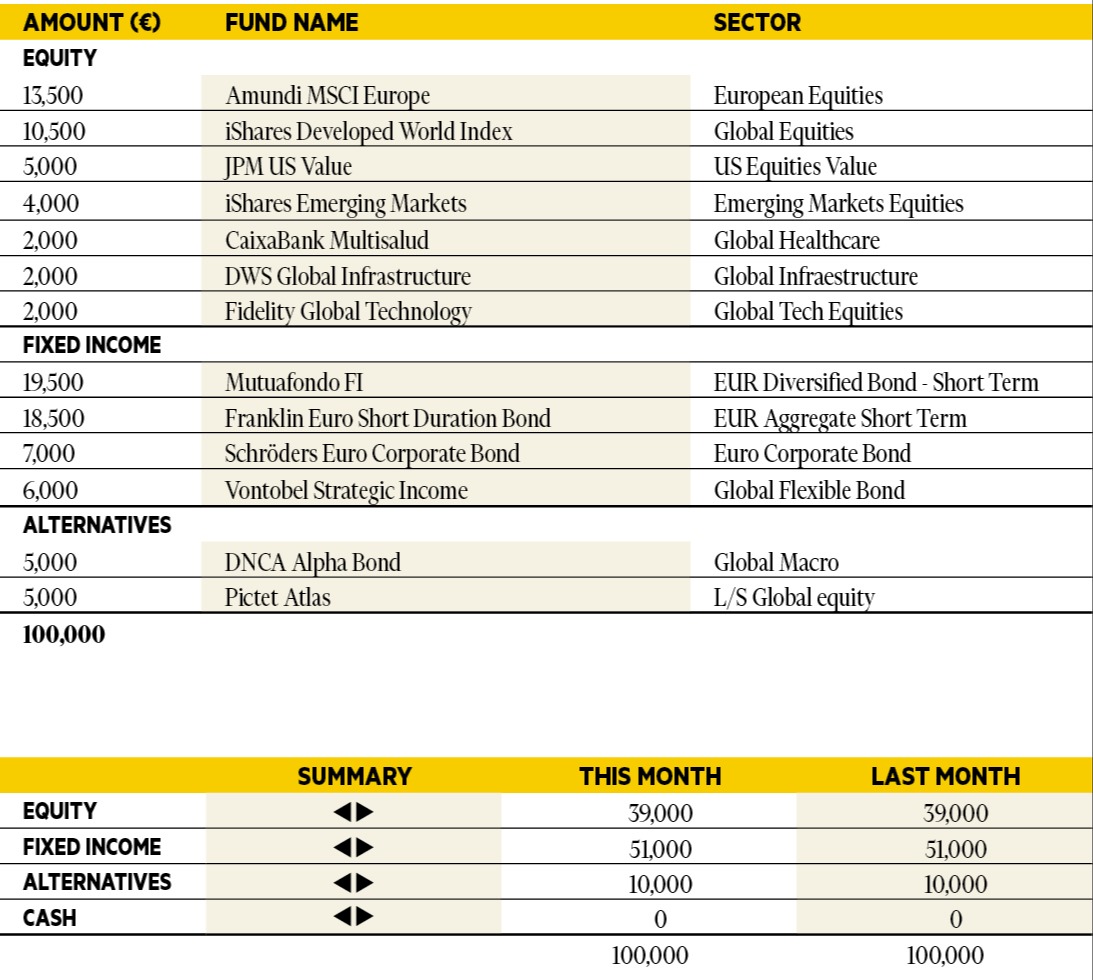

Jorge Velasco

Director of Investment Strategy, CaixaBank Private Banking.

Based in: Madrid, Spain

“In fixed income, markets appear to have overestimated the likelihood of rate cuts in the US, prompting a cautious stance. Exposure to dollar-denominated debt is avoided, and within the Eurozone, there are no active bets on duration or curve positioning. However, a constructive view is maintained on sovereign debt from Italy and Spain, as well as corporate bonds and subordinated financials. On the equity side, geographic diversification remains in place — albeit uncomfortably — while the growing importance of company-specific factors over broader market trends is creating opportunities for alpha through stock selection. In currencies and commodities, oil prices have been volatile due to geopolitical risks, but the base case remains for a new trading range closer to $50 per barrel, potentially even lower in euro terms. The dollar is expected to continue weakening over the long term, though a sideways trend may dominate in the near term. The most critical factor in asset allocation is the recalibration of US financial asset weightings. Economic and corporate data support maintaining an underweight in both US equities and bonds, with a strong preference to minimize dollar exposure. Overall, a cautious and highly tactical approach to risk remains the favored strategy.”

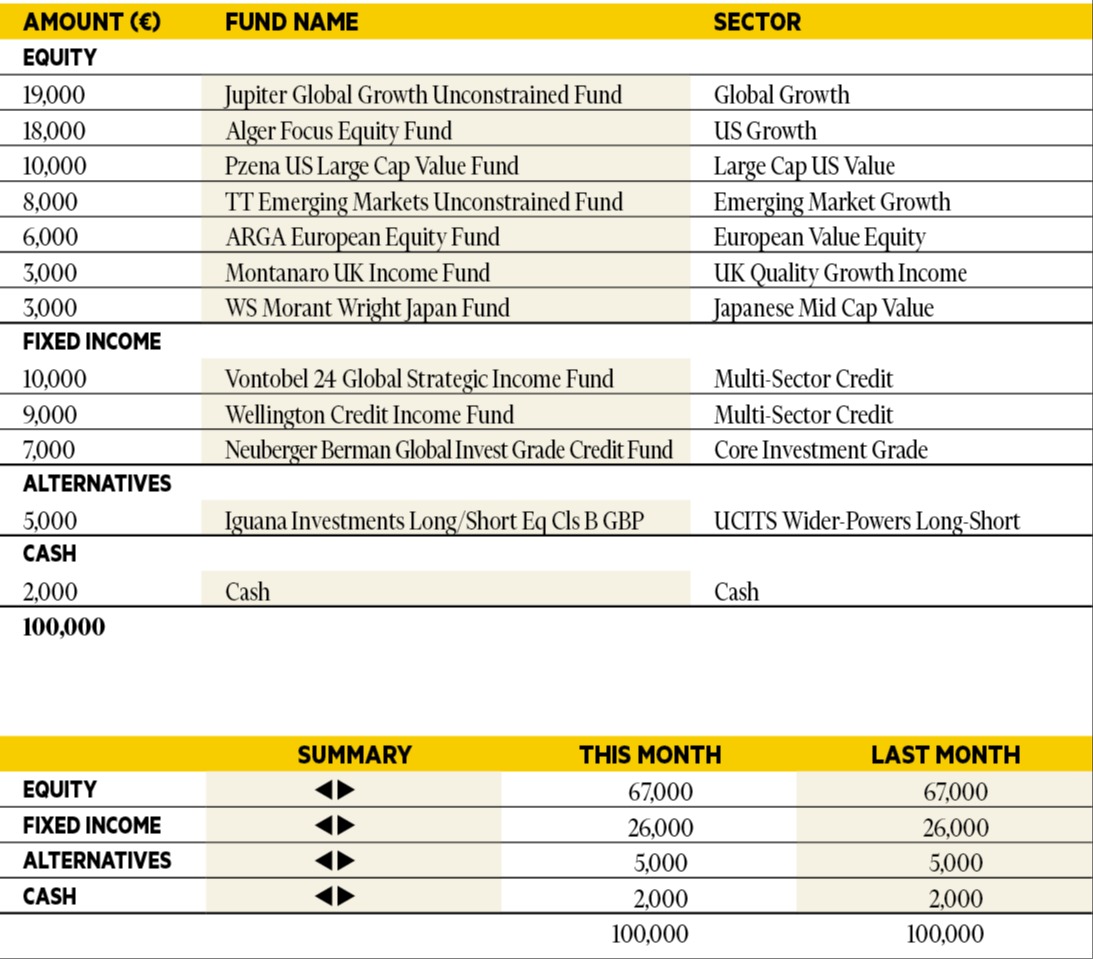

Adam Norris

Portfolio Manager, Colombia Threadneedle Investments.

Based in: London, UK

“Equity markets continued to perform strongly through June, with the S&P 500 having now recovered from April’s lows and has begun reaching new all-time highs. While tariffs and politics continue to fill headlines, technology stocks in US continue to show strong earnings growth, powering the market higher. The best performer was Alger Focus Equity and the worst performer Morant Wright Japan. We have becoming more sanguine on emerging market equities. We still believe US technology stocks will continue to show earnings growth, but the US dollar has begun to falter, which we believe will be most beneficial for emerging markets. We reduced our exposure to Japan as a result.”

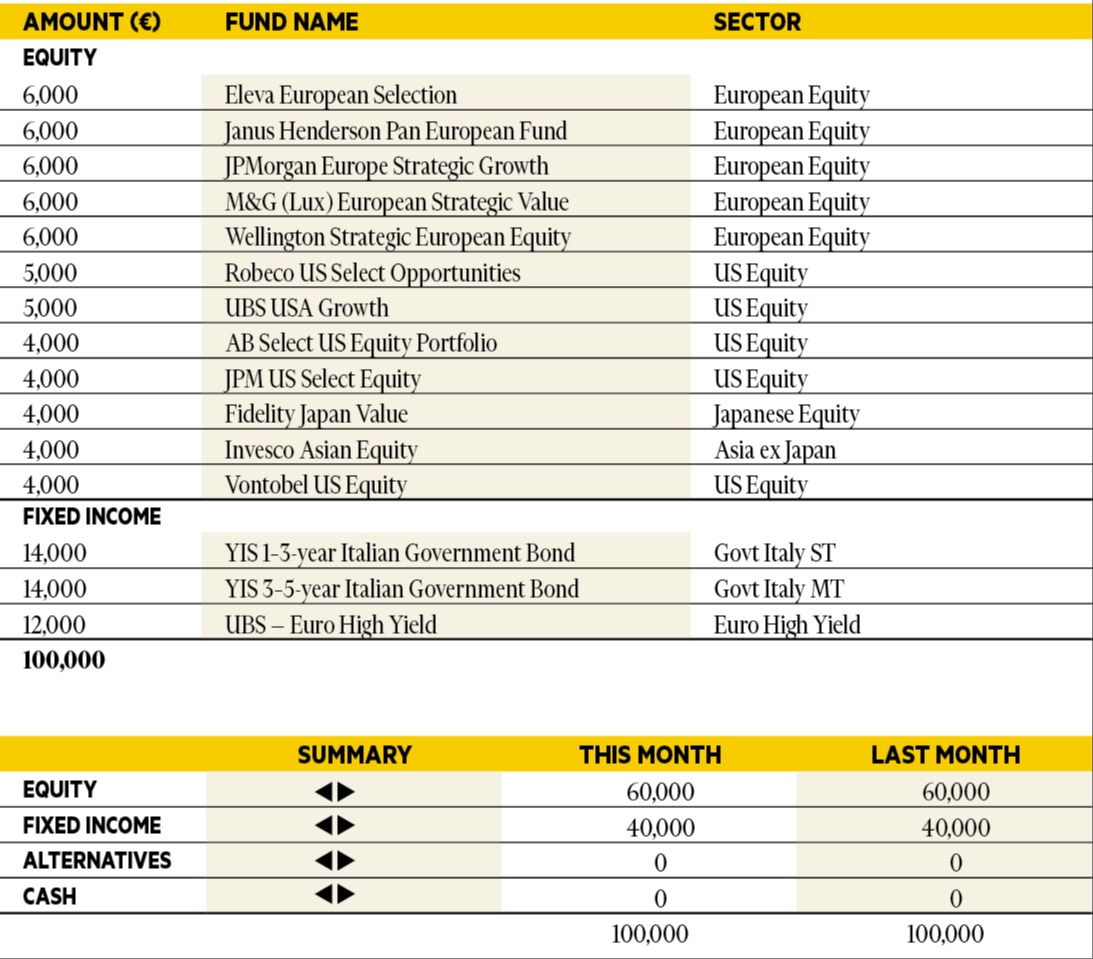

Silvia Tenconi

Multimanager Investments & Unit Linked, Eurizon Capital SGR.

Based in: Milan, Italy

“In June the performance of the portfolio was positive, with UBS USA Growth contributing the most. US equities had a brilliant month, while European markets were down. Credit had a nice rally globally, and government bonds were slightly up in the US and flat in the Eurozone. The US dollar weakened further against the euro, as well as the Japanese yen. During the month, Eurizon Fund vehicles became YIS funds, and the portfolio was updated accordingly. We keep our balanced exposure to equities, high-yield, US dollar and Italian government bonds.”

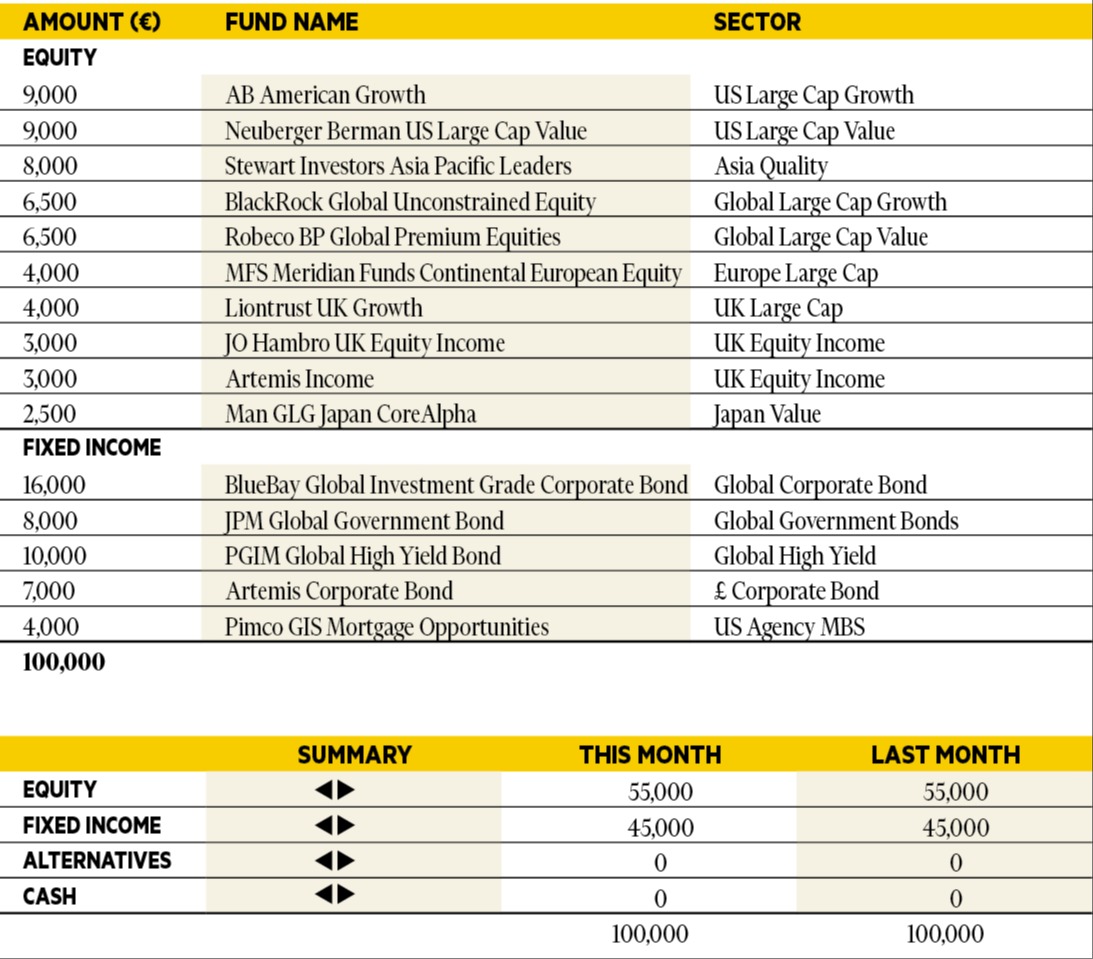

Richard Troue

Fund Manager, Hargreaves Lansdown Fund Managers.

Based in: Bristol, UK

“We have a new addition this month in the form of Pimco GIS Mortgage Opportunities. This fund invests in US agency mortgage-backed securities (MBSs). MBSs offer additional yield over US Treasuries (and global government bonds) of equivalent maturity but with minimal credit risk. The agencies that issue them (Fannie Mae, Ginnie Mae, and Freddie Mac) are more robust than before the Global Financial Crisis. The US housing market is also different, with an undersupply of housing. MBSs have endured headwinds recently from quantitative tightening by the Federal Reserve and selling by banks as their deposits shrank. But these are abating, and it feels like a good time to buy. JPM Global Government Bond has been reduced.”

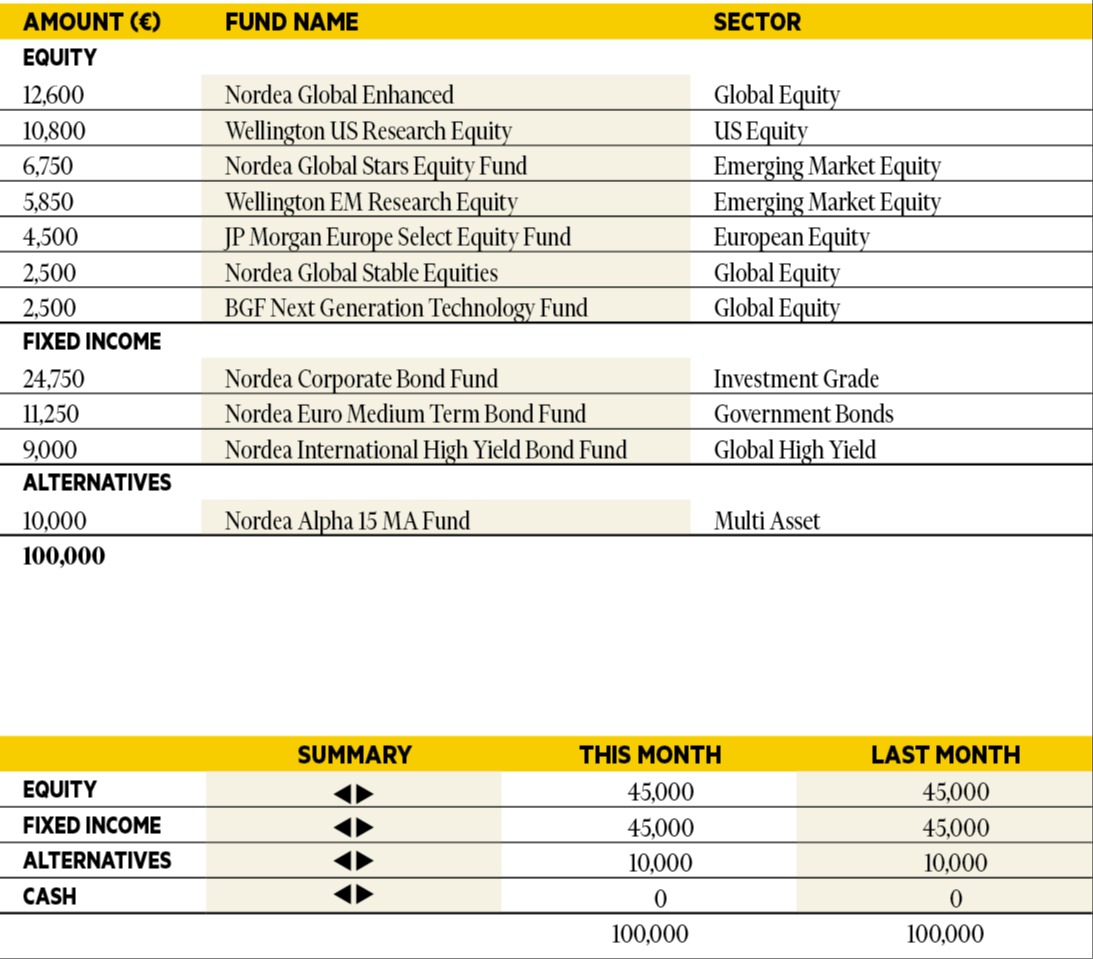

Antti Saari

Chief Investment Strategist, Nordea investments.

Based in: Copenhagen, Denmark

““Peak uncertainty over tariffs and US trade policy is probably behind us, but the outlook is still obscure. Geopolitics is back in the spotlight and the global economy is projected to experience a slowdown, but the US growth outlook is still healthy and so far there are few signs of a substantial slowdown. Improving earnings and a solid enough economic outlook will keep propelling equities higher, barring any negative surprises. However, due to the significant uncertainty in the policy front, we keep our neutral allocation between equities and bonds. Within equities we continue to recommend an overweight in Europe, which will benefit from lower rates and sizeable infrastructure and defence investments going forward.”

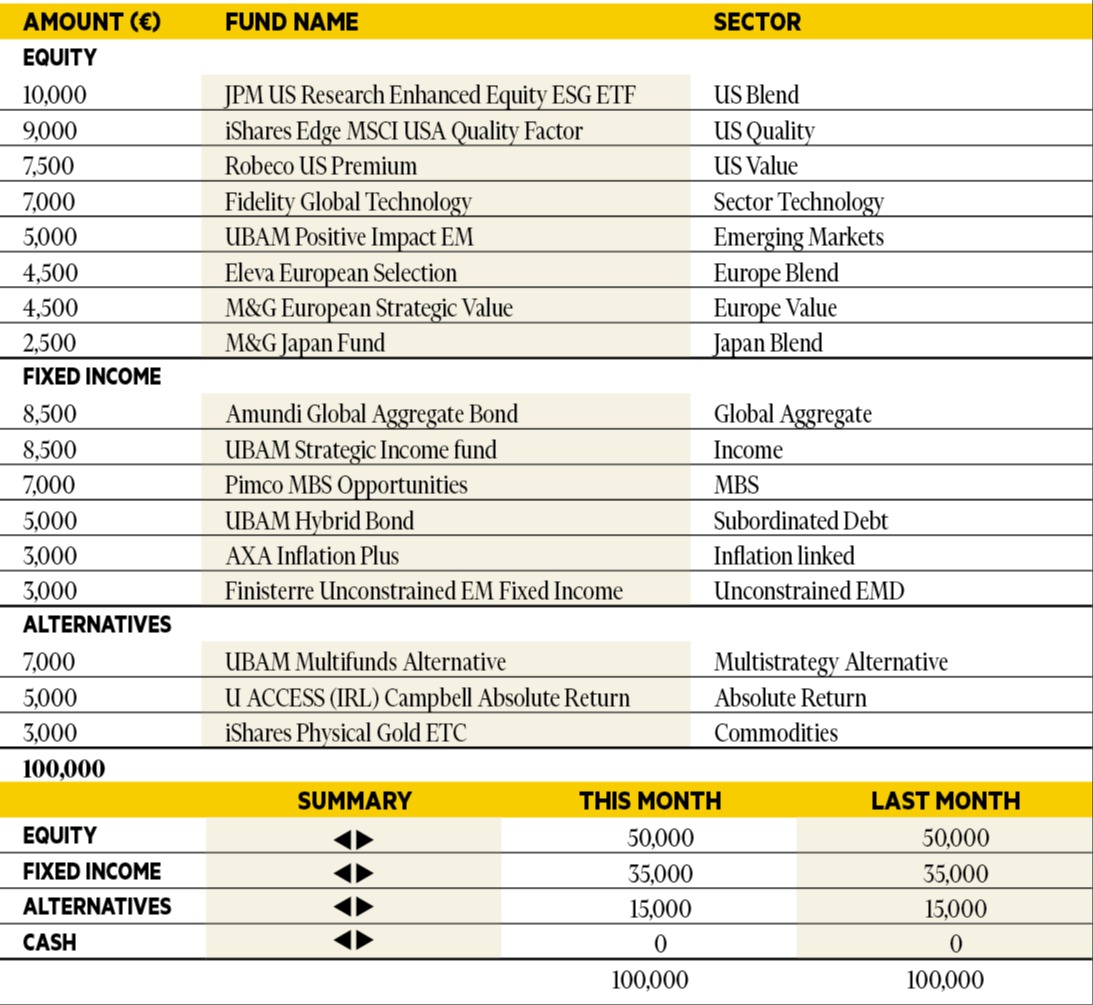

Didier Chan-Voc-Chun

Head of Multi-Management and Fund Research at Union Bancaire Privée (UBP).

Based in: Geneva, Switzerland

“Global equities continued their recovery in June as economic risks and earnings forecast concerns eased. Given the robust performance of the US technology sector, the weakness of the dollar and a resilient US economy, we see upside potential in US earnings projections, which could sustain US equities overall. Consequently, we are increasing our allocation to US equities, indicating our preference for the region for the second half of the year.”