Fund Selection — October 2025

Panel

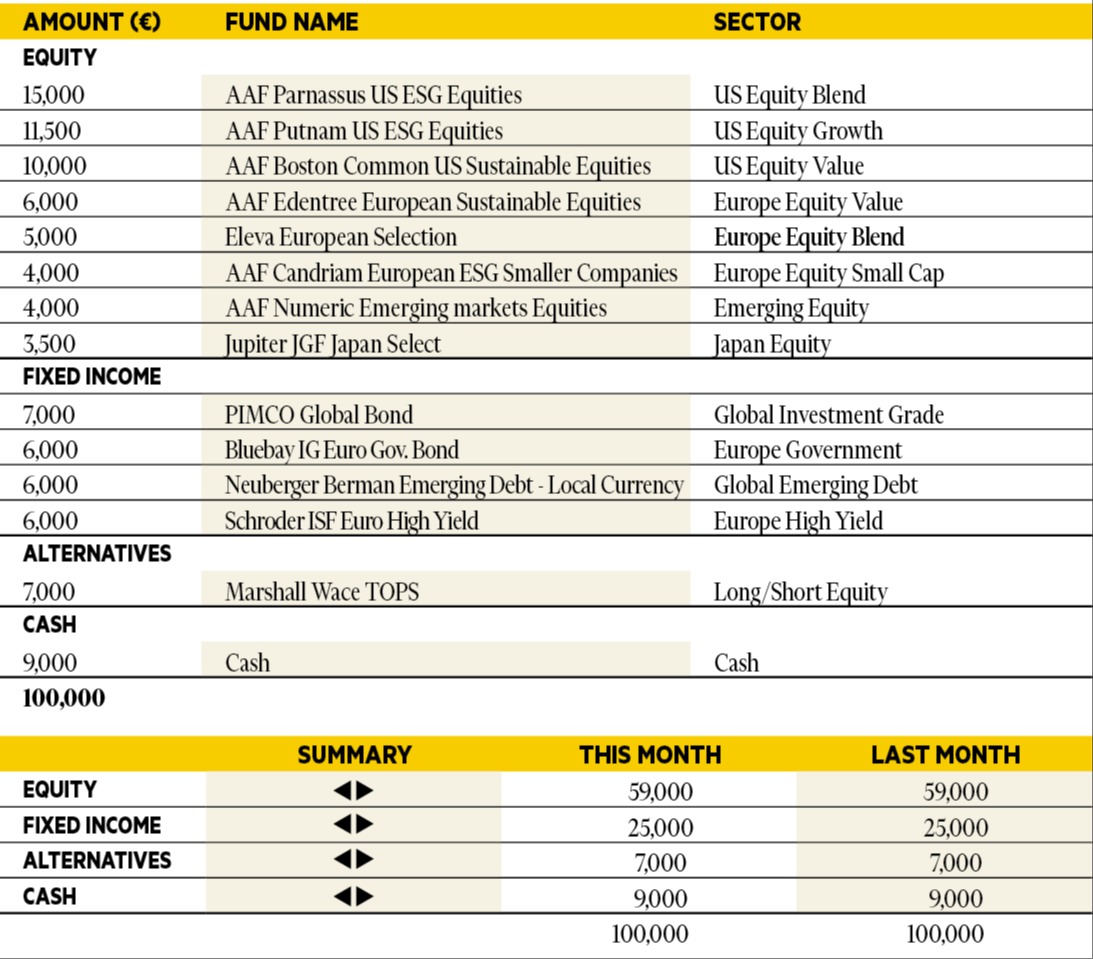

Benjamin Hamidi

Senior portfolio manager, ABN AMRO Investment Solutions.

Based in: Paris, France

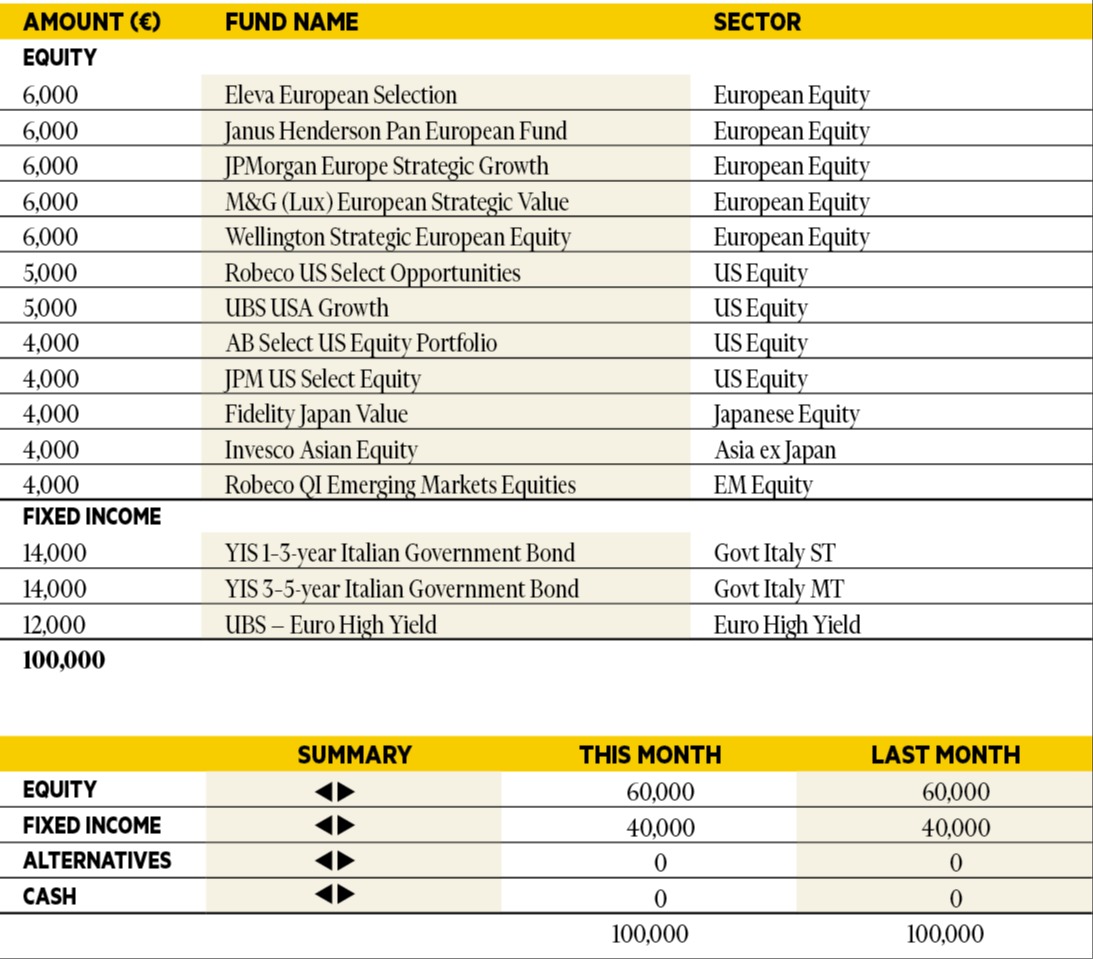

“Consumption is holding up better than expected at this stage and remains resilient. For now, it is not being undermined by a labour market that is slowing but not collapsing, nor by purchasing power potentially eroded by price rises resulting from tariff increases. Risk appetite has also been supported by the Fed’s recent monetary easing, but US core inflation remains above target. Against this backdrop, the current diversified asset allocation remains unchanged. For the time being, a balanced approach is maintained with a preference for equities and, to mitigate the global risk, a cash reserve that can be deployed opportunistically.”

Luca Dal Mas

Senior fund analyst, Aviva Investors.

Based in: London, UK

“During the past month, economic growth showed mixed signals with US second quarter growth revised up to a strong 3.8 per cent annualised pace, driven by consumption and investment, while UK GDP stagnated in July and eurozone PMIs weakened. Inflation pressures persist globally, especially in services, but central banks are diverging in pace and tone of easing, reflecting varied domestic conditions. The Fed cut rates by 25bps, citing labour market risks, with further easing expected. The BoE held rates at 4 per cent, maintaining a cautious stance amid cooling inflation and wage growth. Financial markets remained resilient, with equities rallying and precious metals gaining. In portfolios, we have our positions are largely unchanged as we are comfortable with the current exposure across both equities and fixed income.”

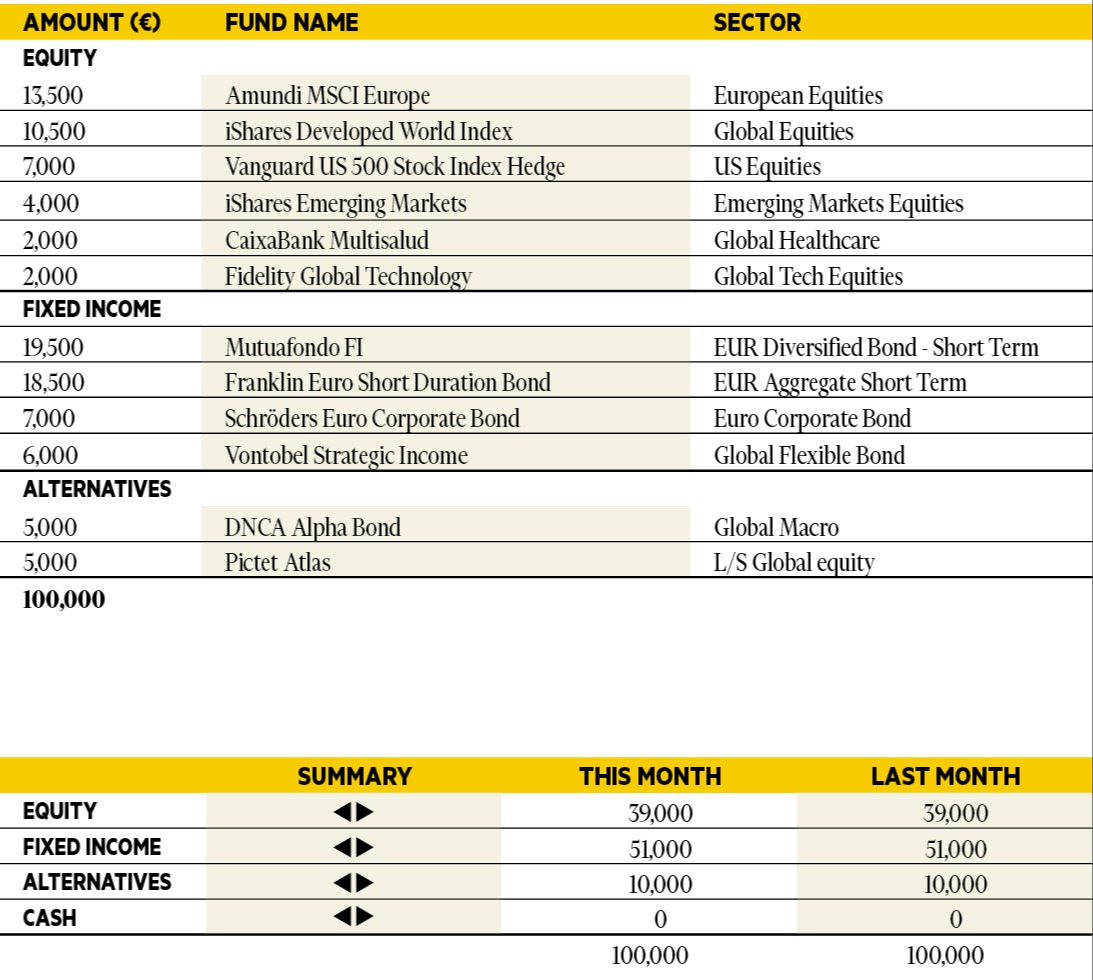

Jorge Velasco

Director of Investment Strategy, CaixaBank Private Banking.

Based in: Madrid, Spain

“Our stance remains cautious — without veering into pessimism — and focused on maximising risk diversification to avoid excessive exposure to the US. Powell’s remarks at Jackson Hole have opened the door to potential rate cuts by the Federal Reserve. The market anticipates fewer rate cuts from the ECB than we do, which gives us a favourable bias towards short-term duration and, more importantly, a steeper yield curve. We maintain a positive outlook on Italian and Spanish sovereign debt, but we prefer corporate bonds and subordinated financial sector instruments. We remain out of French debt, where political instability is expected to worsen. Over the summer, geographic diversification proved beneficial, with strong performance in Japan, China, and our domestic market. Value stocks outperformed growth, despite the rally in US tech. The healthcare sector finally shows signs of recovery after 12 months of underperformance. In addition to our thematic long positions — electrification, power grid infrastructure, and European economic exposure — we are now adding the pharmaceutical sector. When assuming risk, we continue to believe that caution and tactical positioning — even hyper-tactical — are the most appropriate strategies.”

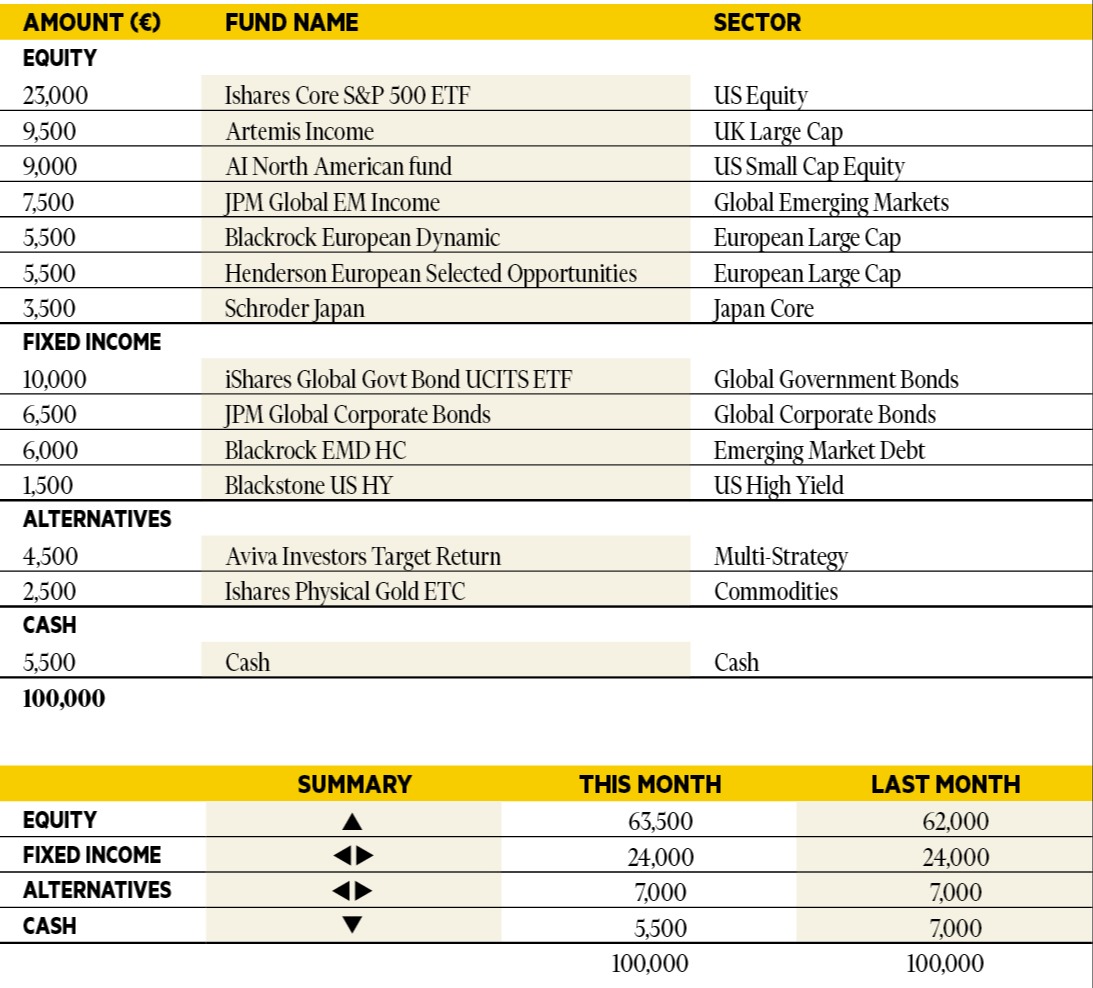

Adam Norris

Portfolio Manager, Columbia Threadneedle Investments.

Based in: London, UK

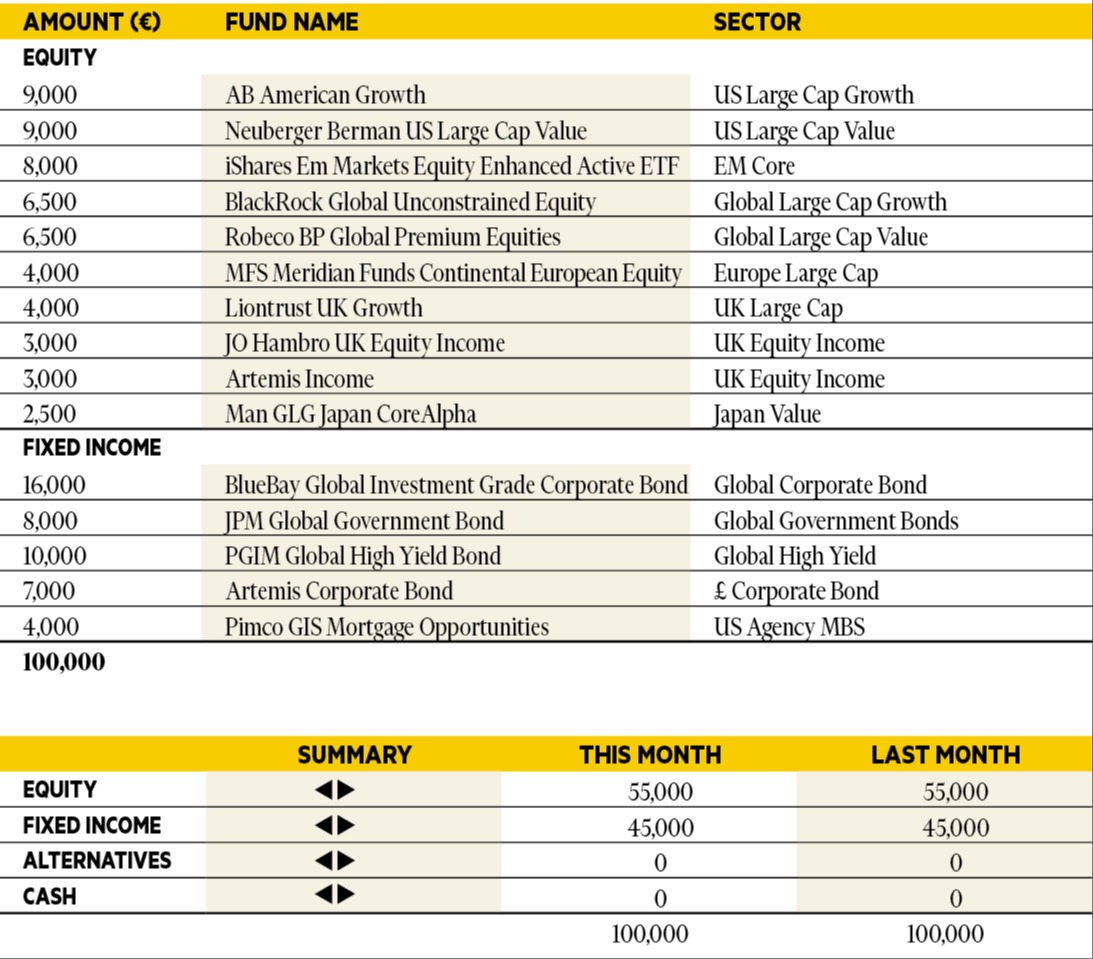

“Risk assets continued to perform strongly through September, with US technology, once again, leading returns. Alger Focus Equity, a US growth-focused portfolio, was up over 9 per cent in September alone, generating a return of over 60 per cent since April’s lows. The weakest performer was Pzena US Large Cap Value, a portfolio containing cheaper but more economically sensitive stocks. Overall, we continue with our pro-risk positioning across the model portfolio. Our selections are unchanged.”

Silvia Tenconi

Multimanager Investments & Unit Linked, Eurizon Capital SGR.

Based in: Milan, Italy

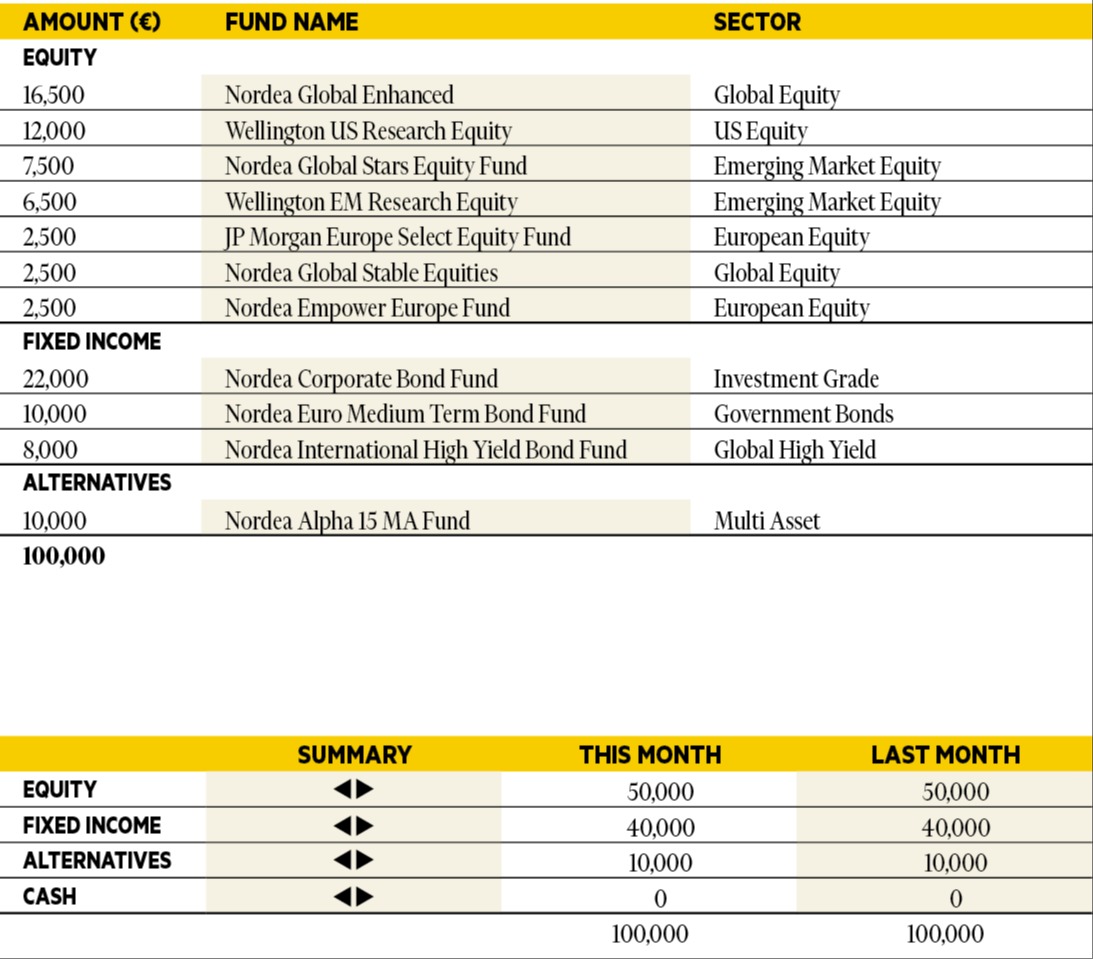

“In September, the performance of the portfolio was positive: all asset classes rose, in a new goldilock scenario: globally, growth is robust or improving, inflation is under control and central banks are normalising monetary policies: the Fed cut interest rates by 25 bps, the ECB is ready to act in case of a slowdown and the BOJ is going to hike rates in response to resilient core inflation. At the end of the month we reduced our exposure to US in favour of emerging markets, selling Vontobel US Equity and buying Robeco QI Emerging Markets Equities.”

Richard Troue

Fund Manager, Hargreaves Lansdown Fund Managers.

Based in: Bristol, UK

“Have the first cracks started to appear in credit markets? This is a question many have asked since the demise of leveraged loans issuer First Brands (a US auto parts supplier). It’s a natural question to ask. There’s always a first domino to fall. That said, this currently looks like a company-specific issue with little, if any, read across to the high-yield bond market. It certainly serves as a reminder that private credit is not risk free and that excessive debt can come back to bite you. As far as our portfolio is concerned, I’m still comfortable with exposure to high-yield bonds via PGIM, an experienced and well-resourced active manager.”

Antti Saari

Chief Investment Strategist, Nordea investments.

Based in: Copenhagen, Denmark

“Global equities continued their solid performance in September. The strongest support came from improving outlooks for the economy and earnings, and a rate cut from the Federal Reserve. We believe these factors will provide tailwinds to equities also going forward. After a strong rally, investors should be prepared for some kind of a near-term correction. However, we believe these mainly represent buying opportunities. We keep equities at an overweight. We continue to recommend an overweight for European equities, as we expect the region to benefit from a cyclical recovery, lower rates, and investments in defence and infrastructure.”

Didier Chan-Voc-Chun

Head of Multi-Management and Fund Research at Union Bancaire Privée (UBP).

Based in: Geneva, Switzerland

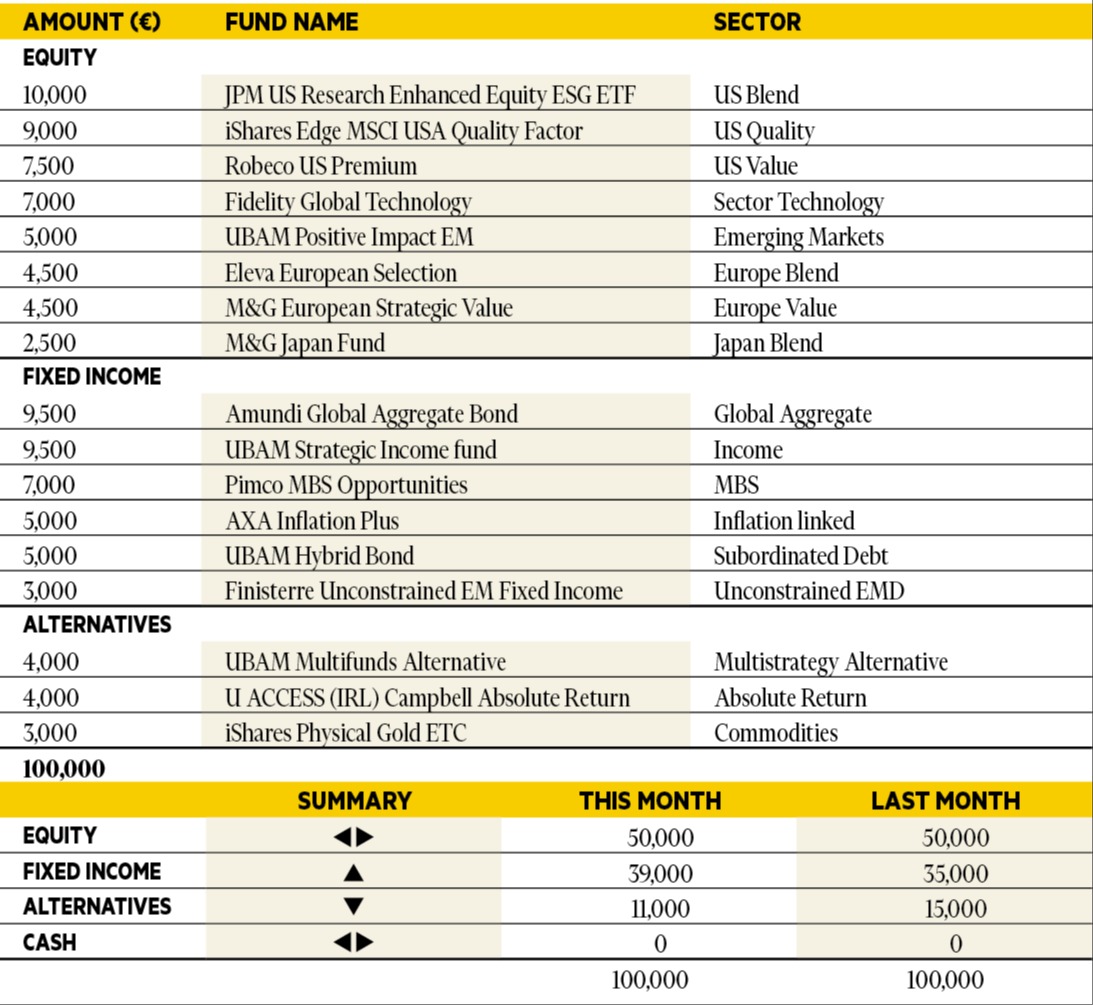

“September saw a rally in both equities and bonds, fuelled by a growing anticipation of Federal Reserve rate cuts. The third quarter of 2025 delivered strong returns across major asset classes, supported by easing trade tensions, sustained enthusiasm for AI, and heightened expectations of monetary easing. In the US, a weak August jobs report, with just 22,000 jobs added and unemployment ticking up to 4.3 per cent, reinforced the case for a quarter-point rate cut to 4.00–4.25 per cent, which was implemented mid-month. This dovish stance boosted equity markets, particularly the tech sector, which was driven by AI momentum in both the US and China. Our conviction on fixed income strategies remained unchanged, favouring high-yield segments like AT1s, while US equities continue to be preferred for their robust technology-driven growth.”