Fund Selection — November 2025

Panel

Benjamin Hamidi

Senior portfolio manager, ABN AMRO Investment Solutions.

Based in: Paris, France

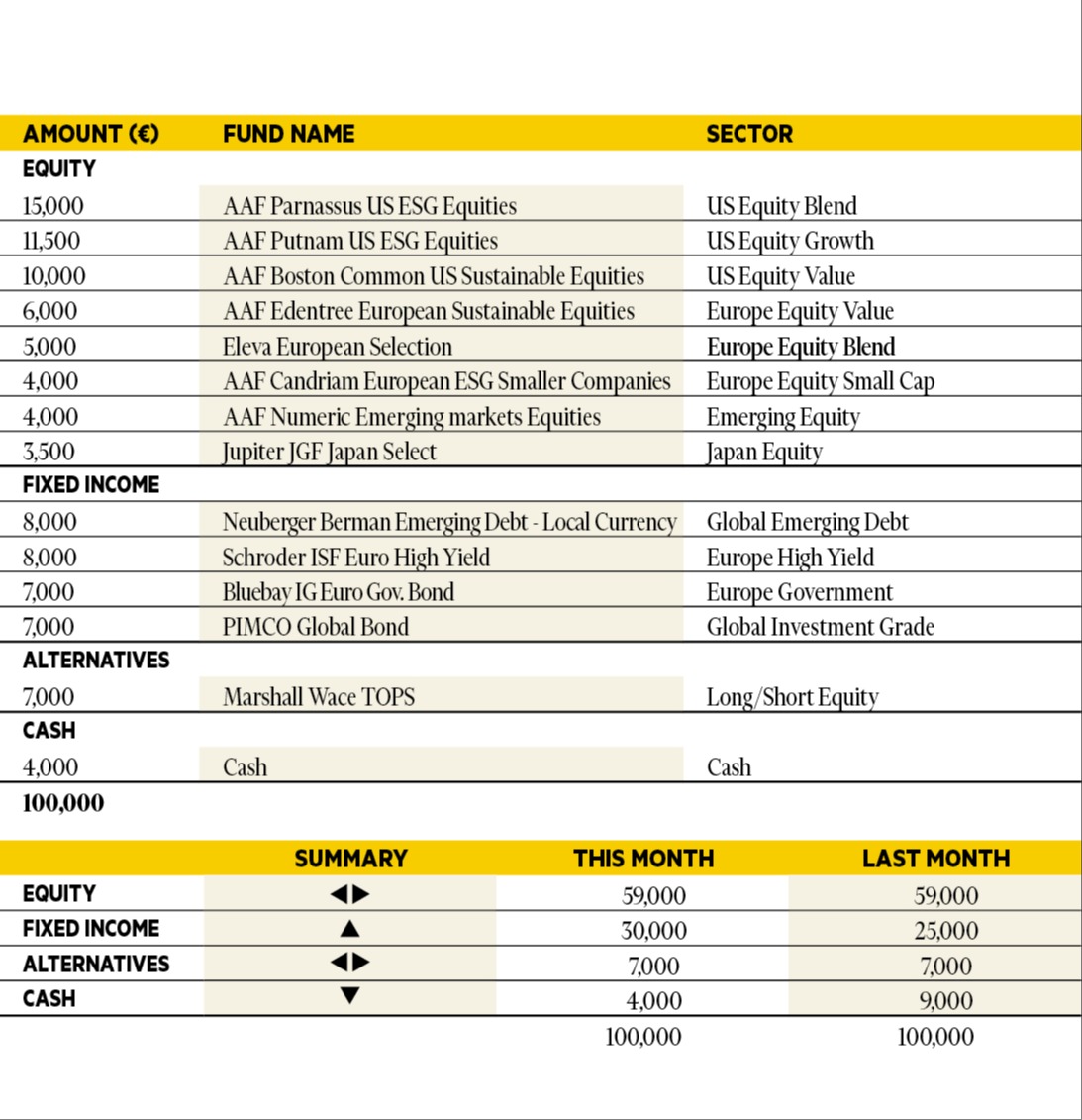

“The global economy is proving resilient: corporate profits and economic activity remain solid, despite weak US consumer confidence and a slowing job market. In emerging economies, inflation is broadly under control, so many central banks feel able to ease monetary policy to support growth, and trade between developing countries. Against this backdrop, we’re maintaining a balanced approach, with an overall stable preference for equities. However, the regional allocation is changing slightly: we are increasing our positions in emerging markets (equities and bonds) and in credit, particularly European high-yield bonds, at the expense of our cash position.”

Luca Dal Mas

Senior fund analyst, Aviva Investors.

Based in: London, UK

“Equities recovered after early month declines, with Asian markets outperforming. Credit spreads widened amid concerns over private credit opacity, with US regional banks suffering a sharp correction. Gold continues its trend and surged mid-month due to geopolitical tensions, but later fell sharply. In the US, core CPI rose marginally — a surprise that reinforced expectations for policy easing. Eurozone inflation remained sticky but stable. Global growth expectations softened slightly, with early survey data revealing broad manufacturing weakness across major economies, while services activity remained resilient. Consumer-driven sectors continue to hold up, while goods production struggles amid trade tensions and higher borrowing costs. In portfolios, we have marginally increased our equity exposure, with a focus towards emerging markets and US equities.”

Jorge Velasco

Director of Investment Strategy, CaixaBank Private Banking.

Based in: Madrid, Spain

“Markets have been volatile this year. Our thesis remains that US equities are overvalued and too concentrated, driven mainly by a handful of AI-related companies. While US stocks rebounded mid-year, recent trends favour other regions, especially Asia. Massive AI investments raise concerns as costs soar and debt grows. Economic policy adds uncertainty: a US–China trade truce contrasts with the Fed’s cautious stance amid inflation and slowing growth. Valuations keep climbing, making convergence uneven. We feel more comfortable now than in June, but risks persist — high prices and concentrated gains make the outlook fragile.”

Adam Norris

Portfolio Manager, Columbia Threadneedle Investments.

Based in: London, UK

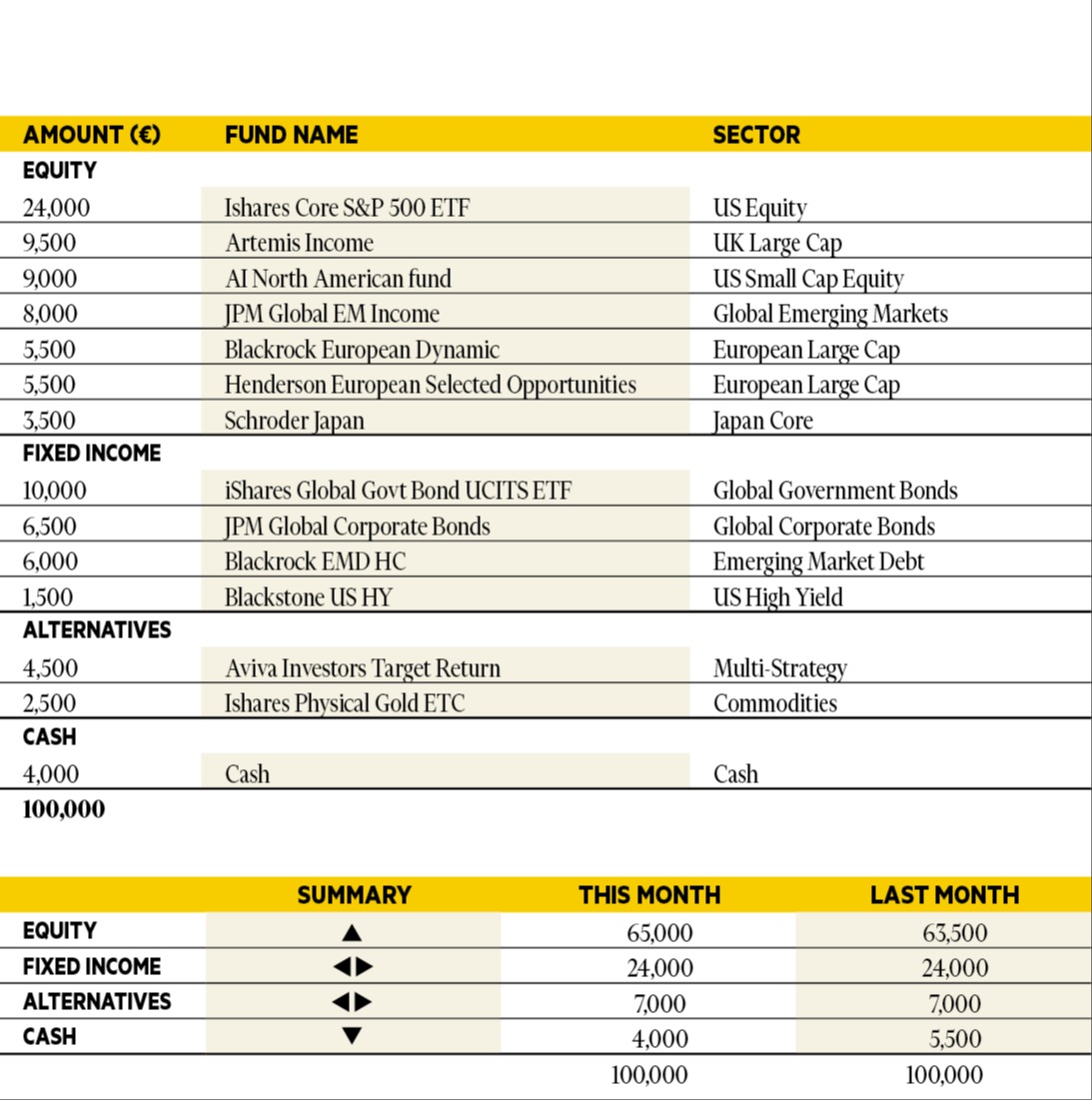

“Risk assets performed strongly in October once again, with Asia and emerging market equity taking the baton from US tech. TT Emerging Markets Unconstrained was up over 10 per cent in October, followed by Alger Focus Equity which returned 5 per cent. All selections were positive in October, but the Vontobel TwentyFour Strategic Income fund produced the lowest return at 0.4 per cent. Overall, we continue with our pro-risk positioning across the model portfolio. Our selections are unchanged.”

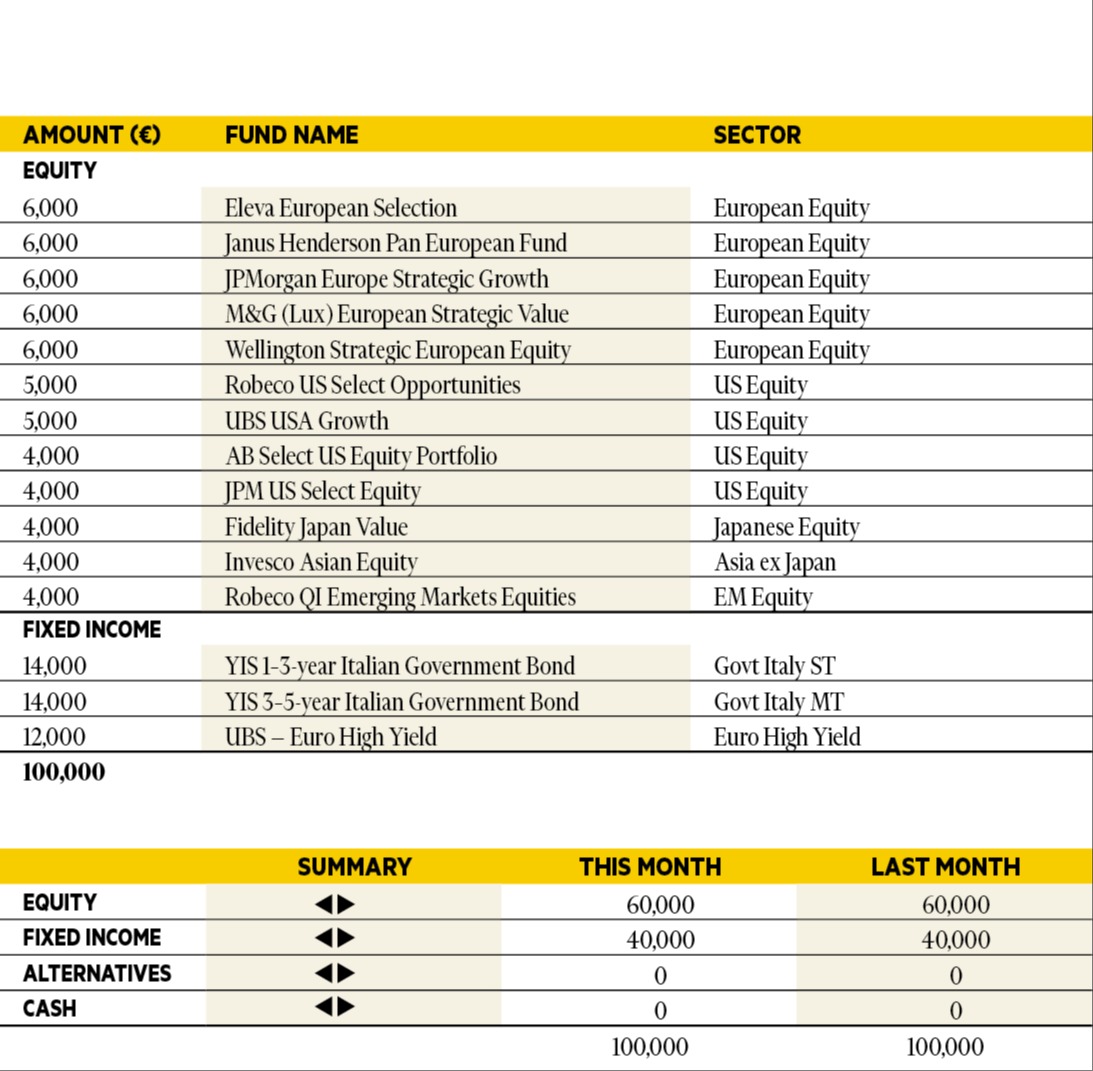

Silvia Tenconi

Multimanager Investments & Unit Linked, Eurizon Capital SGR.

Based in: Milan, Italy

“In October the performance of the portfolio was positive once again. The US reporting season has been good so far — the US government shutdown is still an issue, but is not worrying markets that much, the US dollar is strengthening, government bonds are posting gains alongside IG bonds, while on High Yield there is a bit more fatigue and returns are flattish. Emerging Markets are the standout winners this month. We keep our allocation unchanged, still favouring Italian Govies, Euro High Yield, a globally diversified equity exposure and some US dollar.”

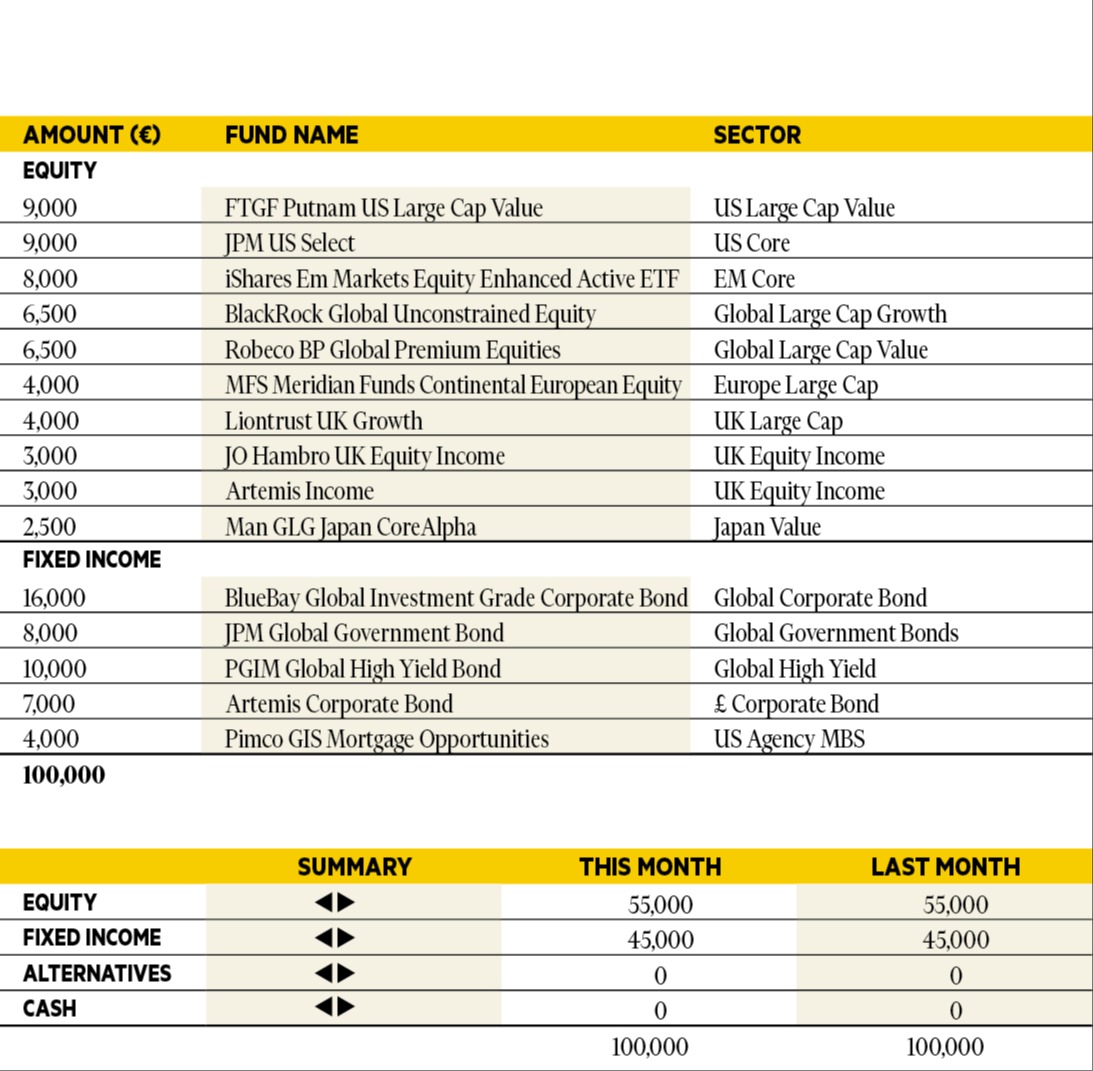

Richard Troue

Fund Manager, Hargreaves Lansdown Fund Managers.

Based in: Bristol, UK

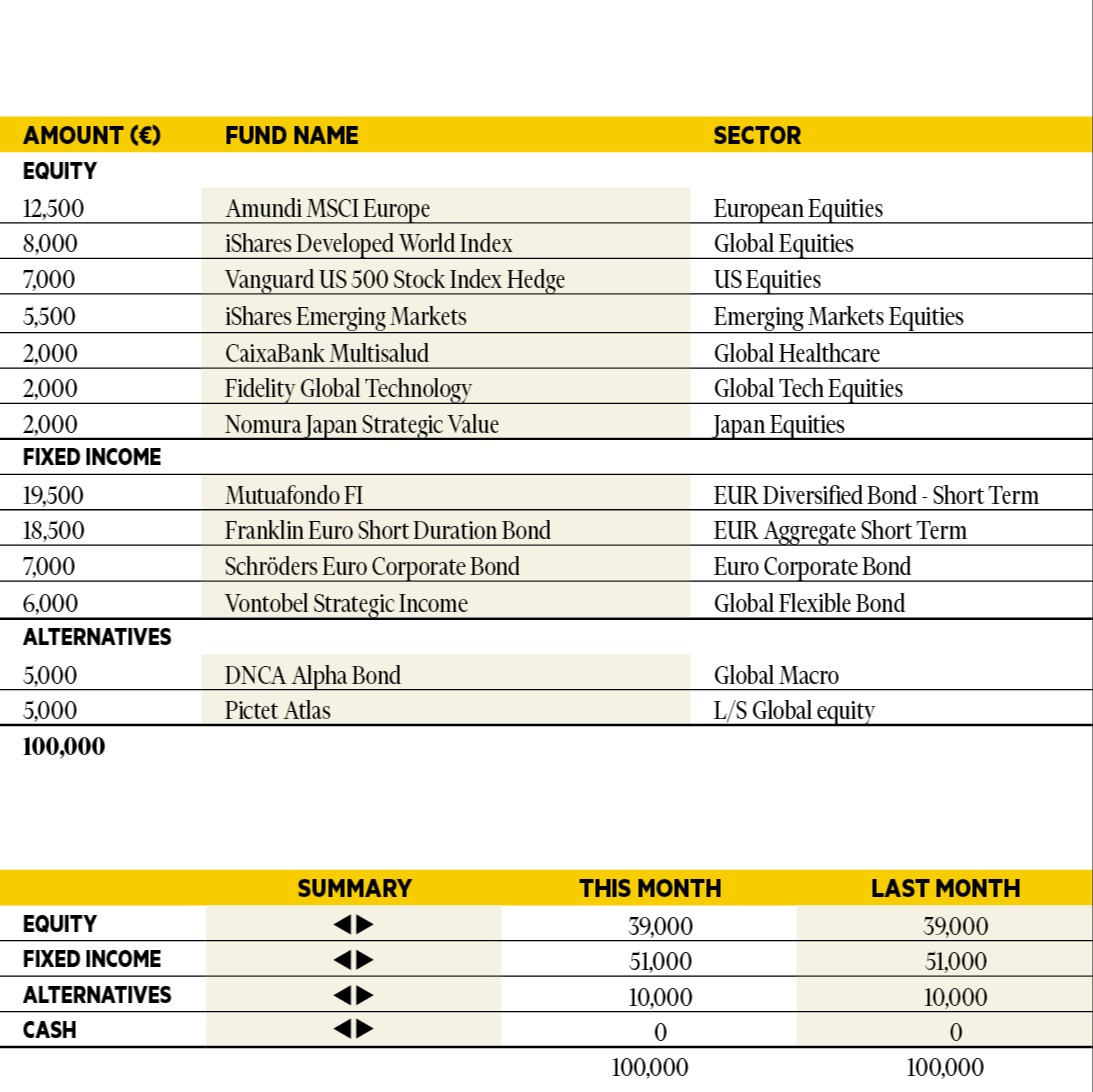

“This month we have made a change to our US investments, adding JPM US Select and FTGF Putnam US Large Cap Value, while removing AB American Growth and Neuberger Berman US Large Cap Value. This should create more of a ‘core’ US portfolio, with more stable relative performance, but still with market-beating returns in the long run. The previous blend of US funds didn’t quite deliver on this front. Given the size and importance of the US market, and the difficultly of outperforming, it’s vital to recognise when something isn’t working and make the necessary changes.”

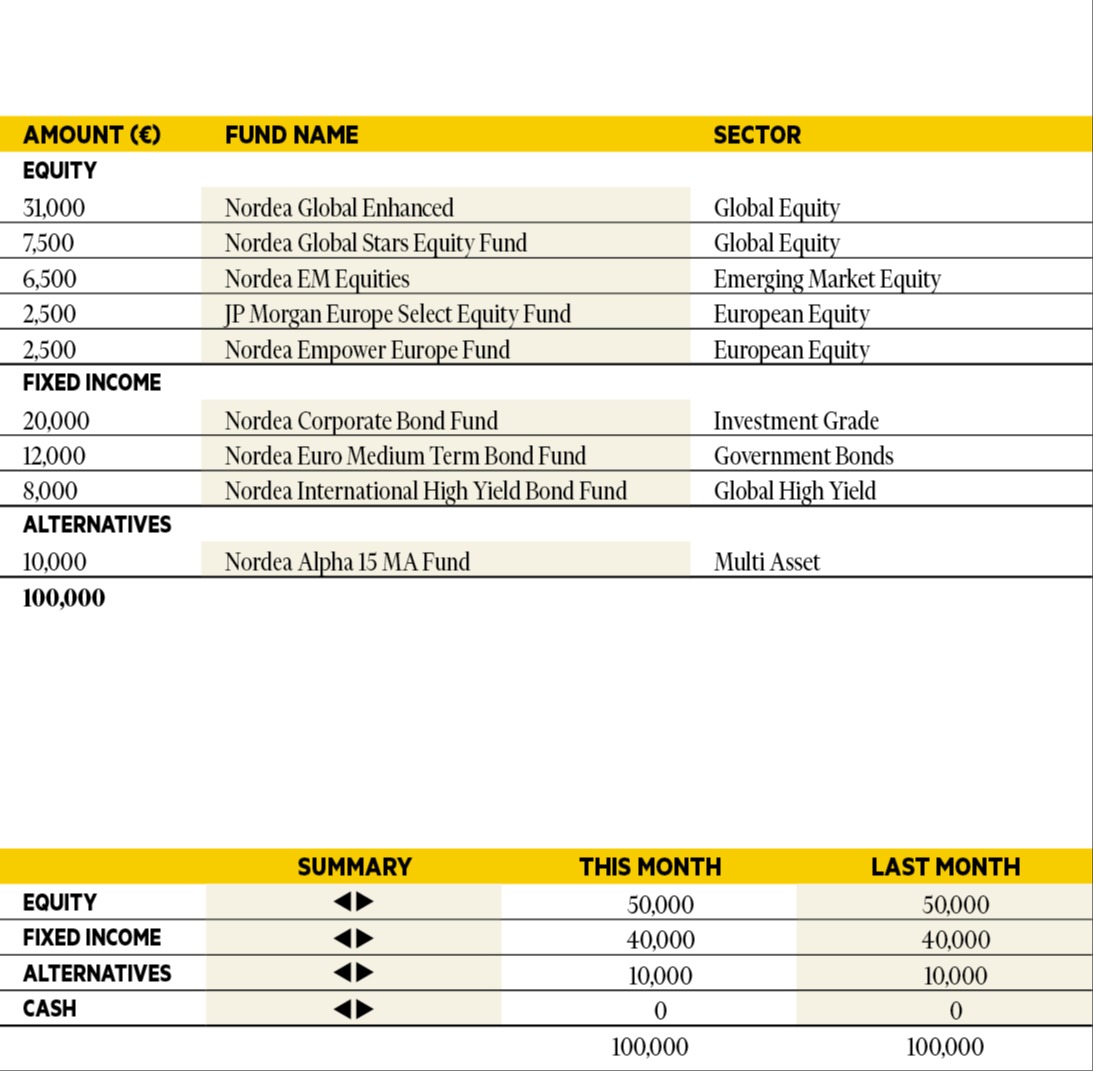

Antti Saari

Chief Investment Strategist, Nordea investments.

Based in: Copenhagen, Denmark

“Global equities continued to rise in October, despite turbulence early in the month. A strong start to the earnings season gave the market a boost. Company reports indicate that growth in consumption and the economy is solid. Good prospects for economic and earnings growth mean that we maintain our overweight in equities versus bonds. Elevated valuations are not a major obstacle in an economy that is growing well. Moreover, investor sentiment remains rather balanced, pointing to reasonable expectations. We continue to recommend an overweight for European equities, as we expect the region to benefit from a cyclical recovery, lower rates, and investments in defence and infrastructure.”

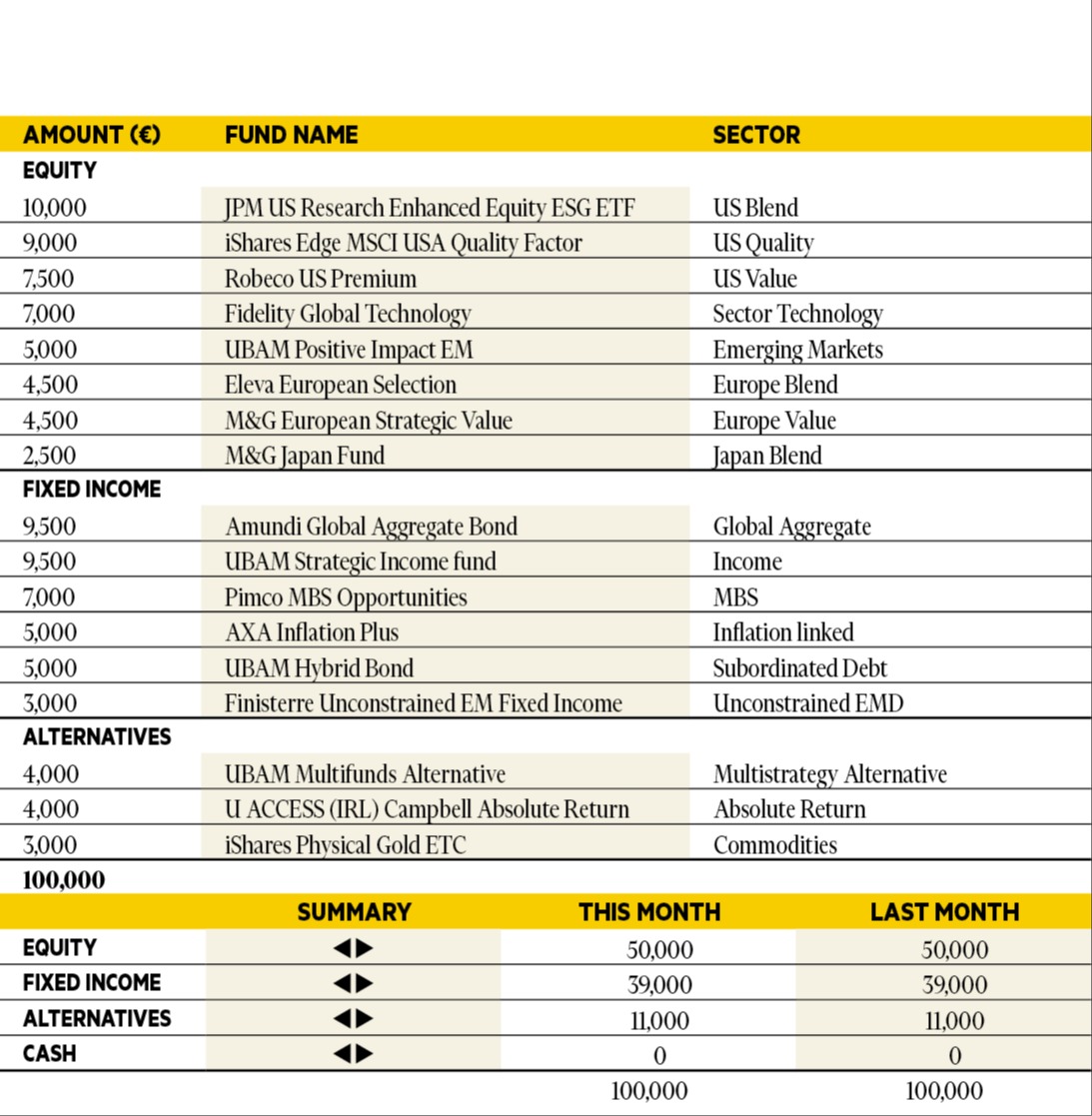

Didier Chan-Voc-Chun

Head of Multi-Management and Fund Research at Union Bancaire Privée (UBP).

Based in: Geneva, Switzerland

“In October, equity markets experienced a significant rally, while their global fixed income counterparts saw a modest decline. The progress in US–China trade negotiations, coupled with the Fed’s quarter-point rate reduction, contributed to global optimism. The US economy remains resilient, despite some signs of softening in the labour market and inflationary pressures that warrant careful consideration. Strength in earnings was once again led by the technology sector, with corporate reporting indicating continued AI infrastructure-related spending. Against this backdrop, we maintain our core conviction on US equities, which are preferred given their robust technology-driven growth, and favour high-yielding segments in fixed income exposures.”