Fund Selection — September 2025

Panel

Benjamin Hamidi

Senior portfolio manager, ABN AMRO Investment Solutions.

Based in: Paris, France

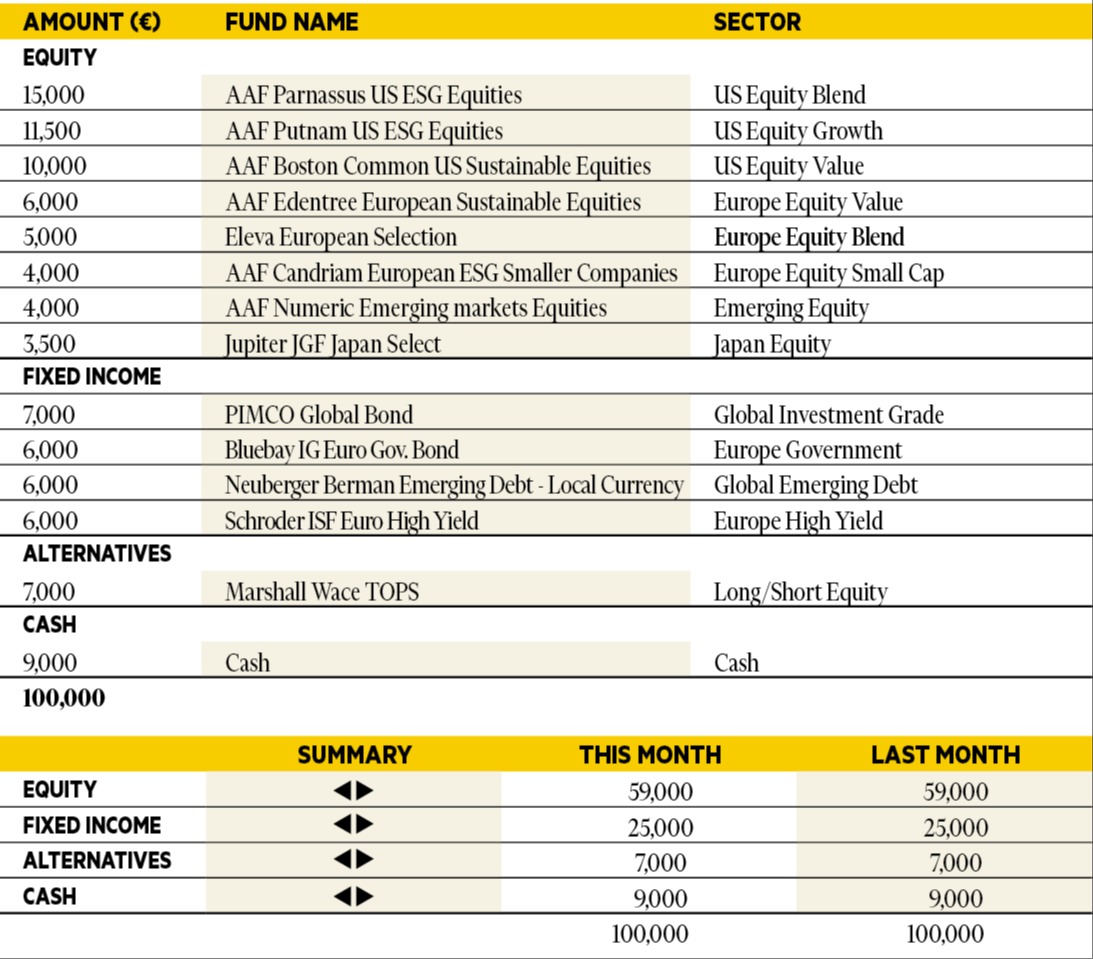

“Activity and consumption in the US remain resilient overall. Protectionist measures are having a moderate impact on the global economic situation, and risk appetite remains high in the markets. The slow transmission of the tariff shock could support continued earnings expansion in the short term. Fed chair Jay Powell has signalled a change in the risk hierarchy, making a rate cut more likely in the short term. In this context, the current moderate diversified asset allocation remains unchanged. We are closely monitoring the impact of tariff changes and how markets perceive the sustainability of the fiscal deficit dynamic (in Europe and the US).”

Luca Dal Mas

Senior fund analyst, Aviva Investors.

Based in: London, UK

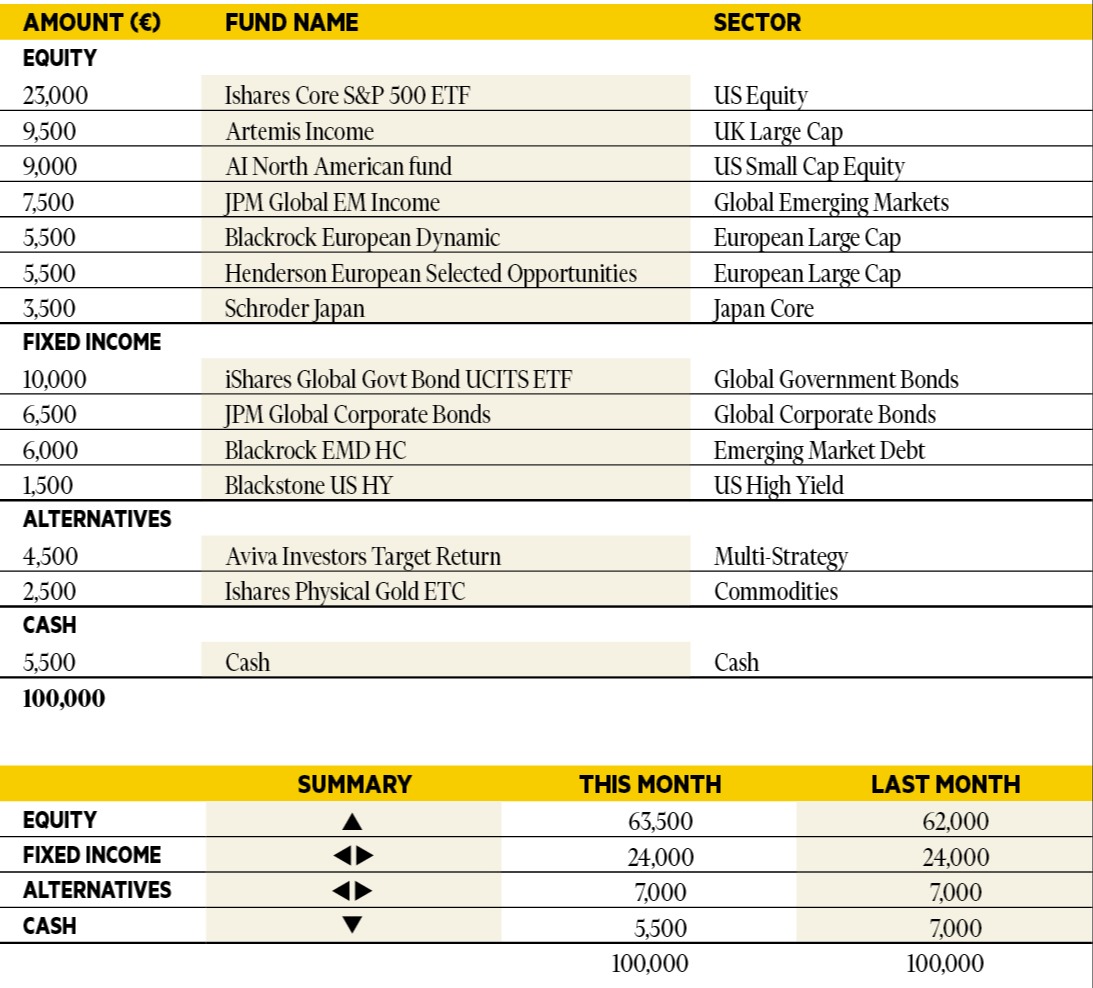

“August saw positive momentum in developed equity markets, with US indices posting gains while European markets lagged. Manufacturing PMIs showed signs of recovery in the US, driven by a rebound in new orders, though global manufacturing remained under pressure due to fading pre-tariff demand and ongoing trade uncertainties. Services PMIs continued to lead global growth, supporting broader economic resilience. The Federal Reserve faces growing pressure to cut rates amid softening labour data, although inflation — partly driven by tariffs — remains a concern. Meanwhile, the European Central Bank and Bank of England held rates steady, with limited easing priced in, reflecting persistent inflation and resilient labour markets. In portfolios, we have slightly increased equity exposure, focusing on the US and, to a lesser extent, emerging markets.”

Jorge Velasco

Director of Investment Strategy, CaixaBank Private Banking.

Based in: Madrid, Spain

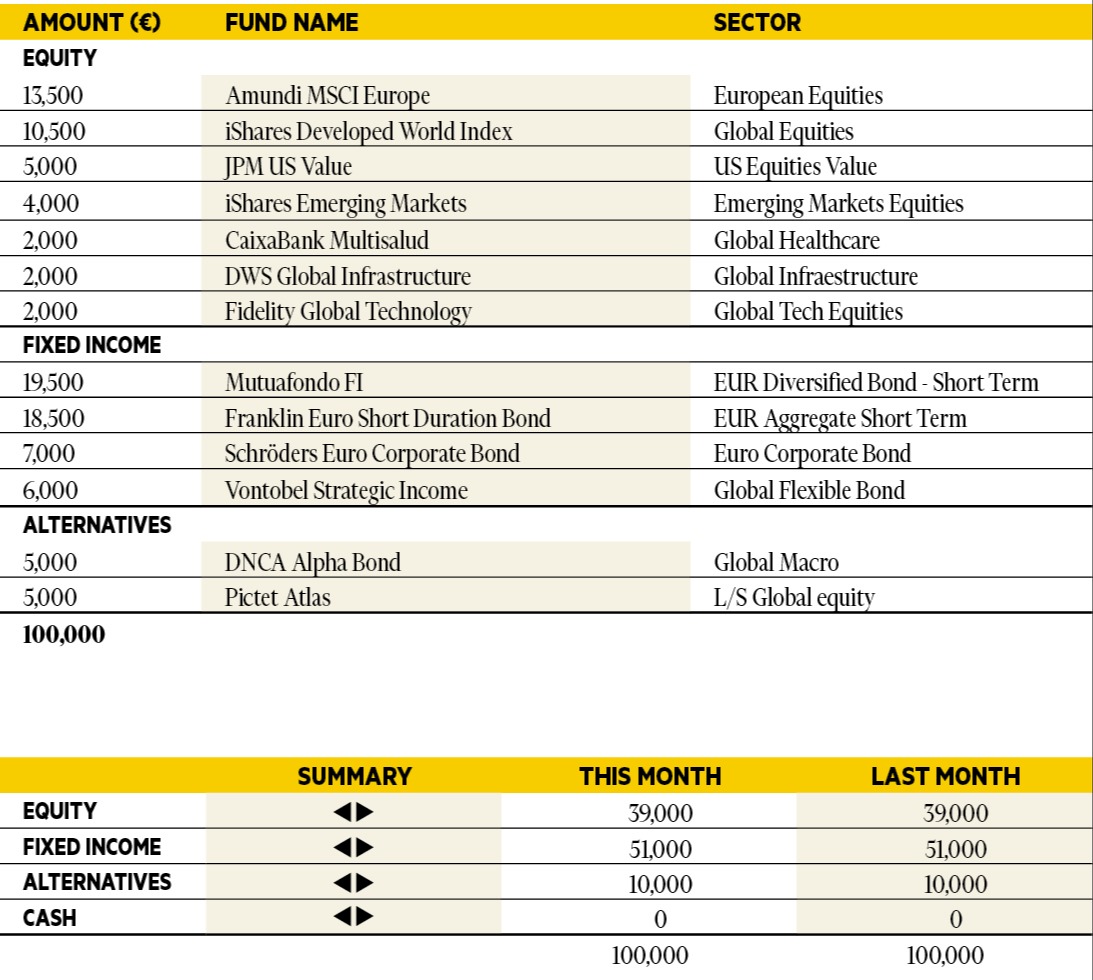

“We remain cautious and focused on maximising risk diversification to avoid excessive exposure to the US. The Fed has opened the door to potential rate cuts, while the market anticipates fewer cuts from the ECB than we do, giving us a favourable bias towards short-term duration and a steeper yield curve. Our outlook remains positive on Italian and Spanish sovereign debt, but we favour corporate bonds and subordinated financial sector instruments. In equities, geographic diversification has paid off, with strong performance in Japan, China and our domestic market. Value stocks have outperformed growth, despite the US tech rally. The healthcare sector appears to be rebounding after 12 months of underperformance. We’re adding the pharmaceutical sector to our thematic long positions — electrification, power distribution networks and exposure to the European economy. We believe the US dollar has entered a prolonged period of weakness, but due to the situation in France, we prefer to express this view through currencies other than the euro — particularly Asian currencies.”

Adam Norris

Portfolio Manager, Columbia Threadneedle Investments.

Based in: London, UK

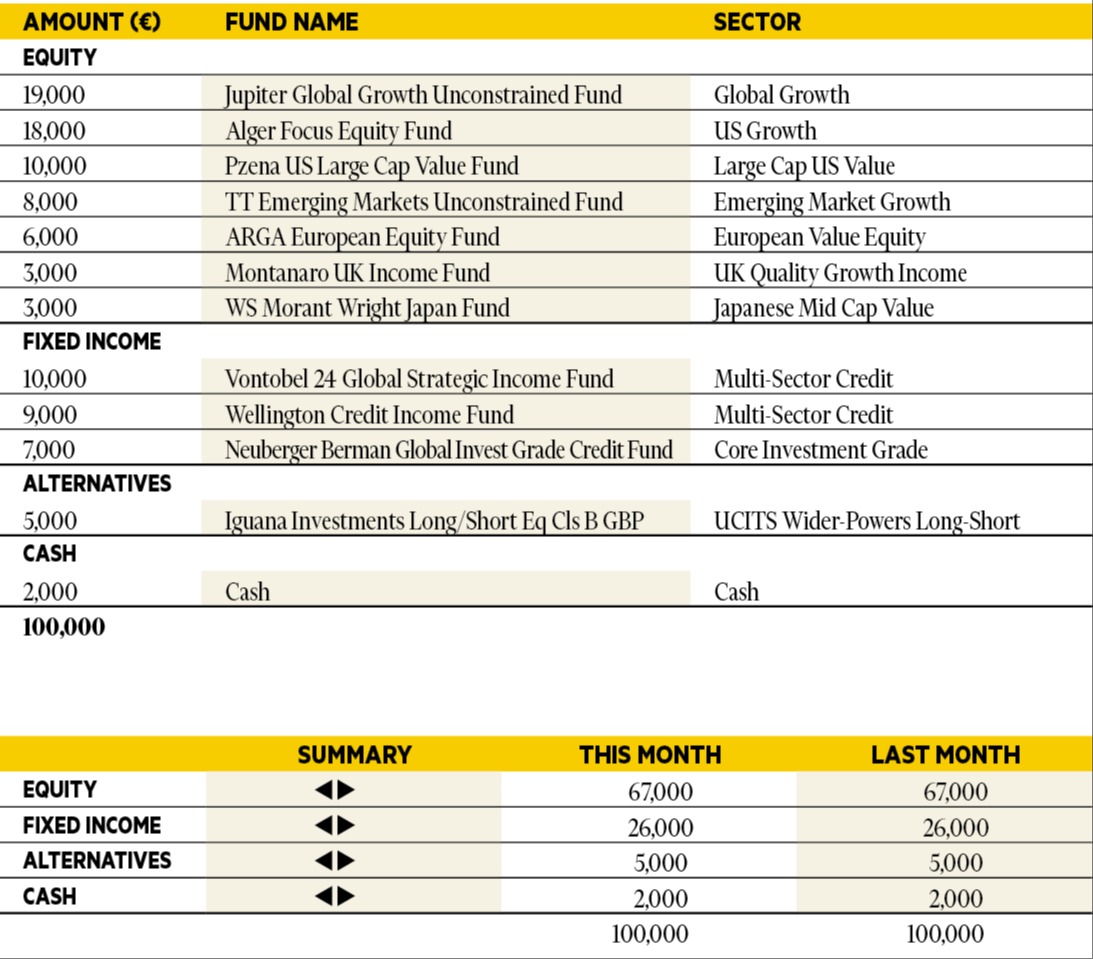

“Equity markets continued to push higher through August, with the market broadening from its narrow rally. Japanese equities led the charge spurred on by the recent election results and continued corporate reform. As a result, Morant Wright Japan Fund was the strongest performer in our model portfolio up 5.9 per cent. We continue our pro-risk asset positioning with an overweight to both equities and credit. Within this, we favour US equities, emerging market equities and credit funds with an allocation to high yield.”

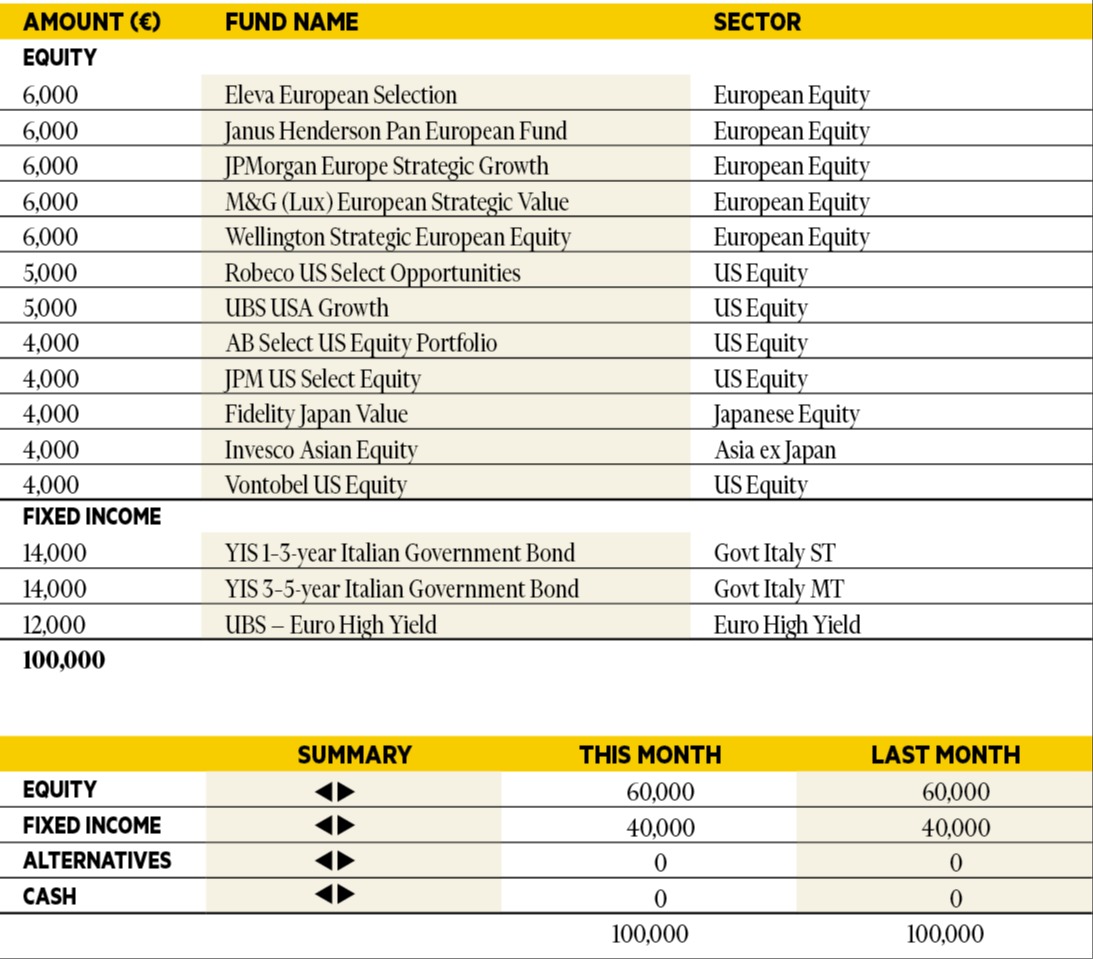

Silvia Tenconi

Multimanager Investments & Unit Linked, Eurizon Capital SGR.

Based in: Milan, Italy

“In August the performance of the portfolio was flat, with Fidelity Japan Value contributing the most. Equity markets rose; credit had a positive month in the US but was flat in Europe; and government bonds were mildly negative in the Euro area and positive in the US. The US dollar weakened while the yen was broadly flat versus the Euro. US GDP data was strong while Jay Powell’s speech at Jackson Hole was more dovish than expected. We keep our balanced exposure to Equities, High Yield, US dollar and Italian government bonds.”

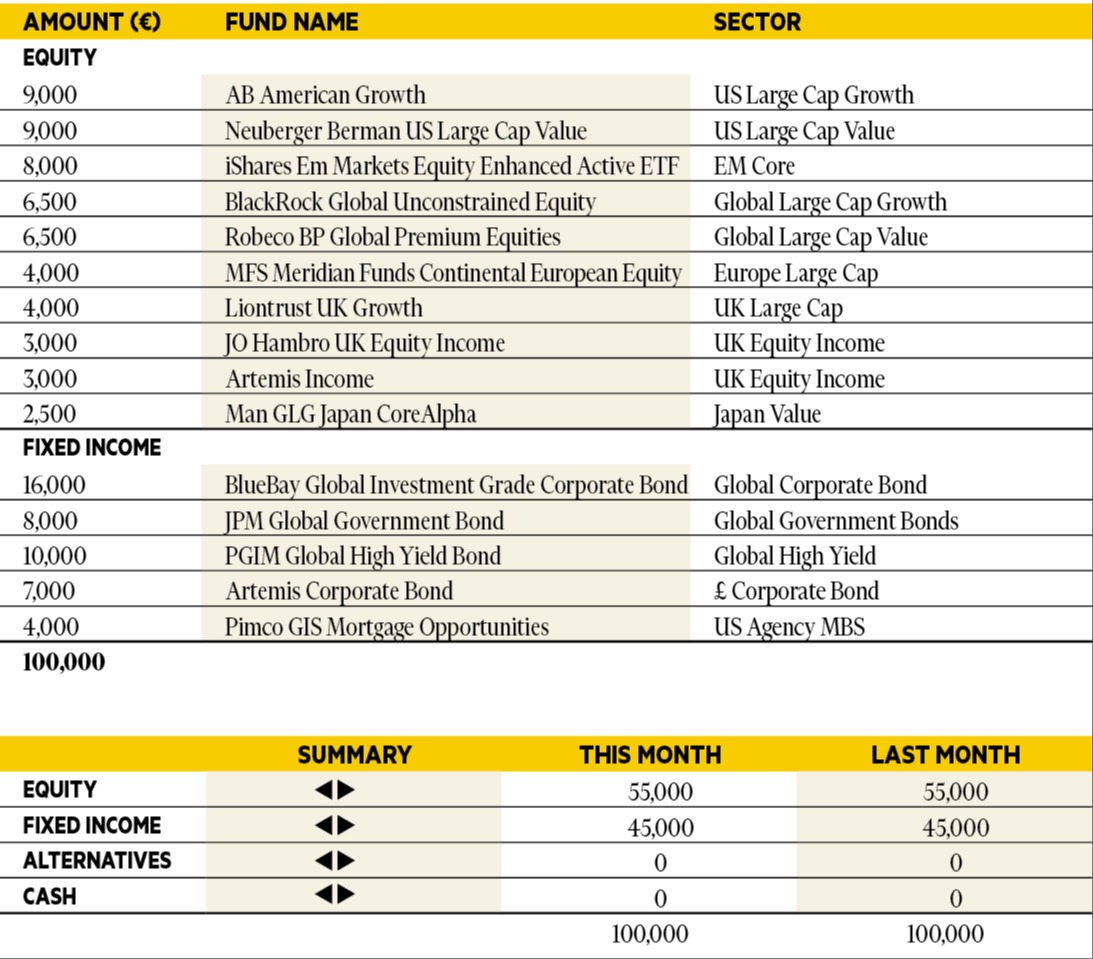

Richard Troue

Fund Manager, Hargreaves Lansdown Fund Managers.

Based in: Bristol, UK

“I’ve added iShares Emerging Markets Equity Enhanced Active UCITS ETF to the portfolio this month. It invests across emerging markets equities using a quantitative approach. The team running it has collated a huge library of ‘alpha signals’ that can identify stocks likely to outperform. The portfolio has no significant country or sector biases, meaning stock selection should be the dominant driver of performance. It’s designed to have a low Tracking Error and generate modest excess returns on a relatively consistent basis. As such it’s ideal as a ‘core’ emerging markets investment. It has replaced Steward Investors Asia Pacific Leaders following the resignation of that funds managers.”

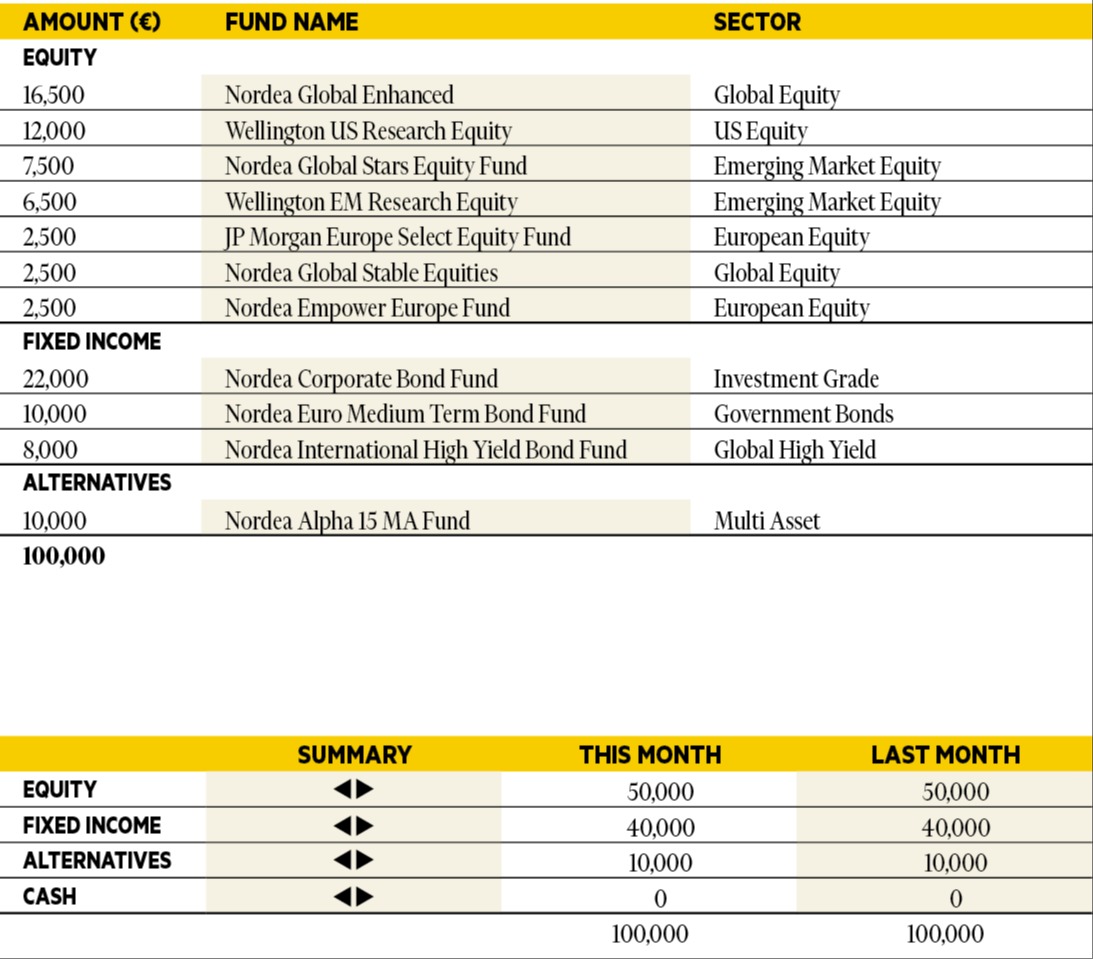

Antti Saari

Chief Investment Strategist, Nordea investments.

Based in: Copenhagen, Denmark

“After a brief setback in early August, equities resumed their uptrend. A strong earnings season in the US and increased expectations of a Fed cut in September boosted risk appetite. While growth in the US has slowed, the overall macro and earnings backdrop remains strong enough to support equities going forward. Equity valuations have crept up since last spring, but stocks are still more attractive than bonds in an environment of moderate growth and an expected pick-up next year. Although investors have increased their equity exposure lately, positioning is still light and sentiment slightly cautious. We therefore believe that the equity market rally has further to go and keep the recommendation to overweight equities versus bonds. We downgrade investment grade bonds and upgrade government bonds to neutral as credit spreads have narrowed to low levels and yields on government bonds grown increasingly attractive.”

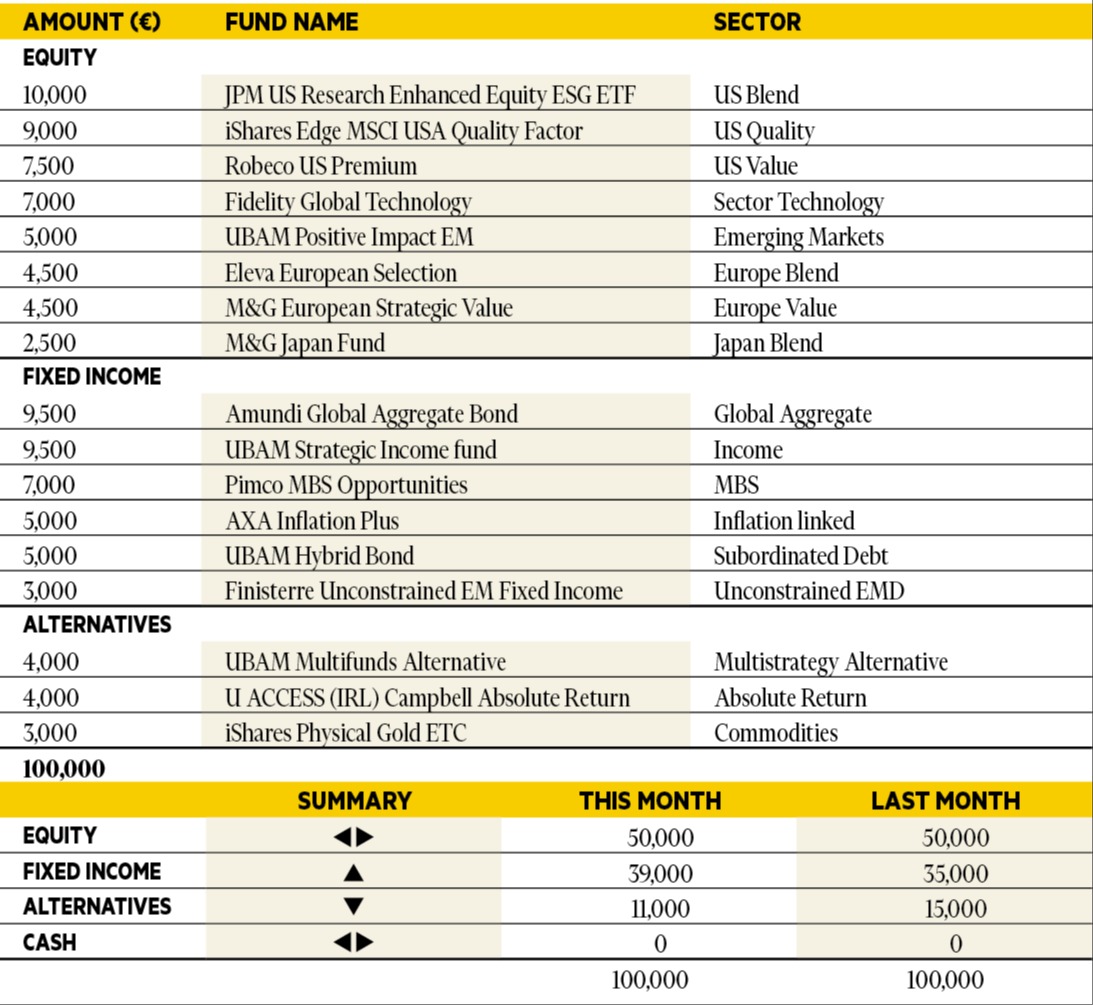

Didier Chan-Voc-Chun

Head of Multi-Management and Fund Research at Union Bancaire Privée (UBP).

Based in: Geneva, Switzerland

“In August, global activity remained resilient and inflation stayed in check, supporting investor optimism despite softer US labour market data and a recent, subdued report on AI. Strong corporate earnings and the prospect of lower interest rates drove positive returns in global equities. Meanwhile, global bond markets delivered mixed results, influenced by economic data and political developments. With increased convictions on fixed income supported by a downward revision to the target for 10-year Treasury yields, we boosted allocations to emerging market debt and our global fixed income exposure, while trimming hedge fund allocations.”