Fund Selection — December 2025

PWM

Benjamin Hamidi

Senior portfolio manager, ABN AMRO Investment Solutions.

Based in: Paris, France

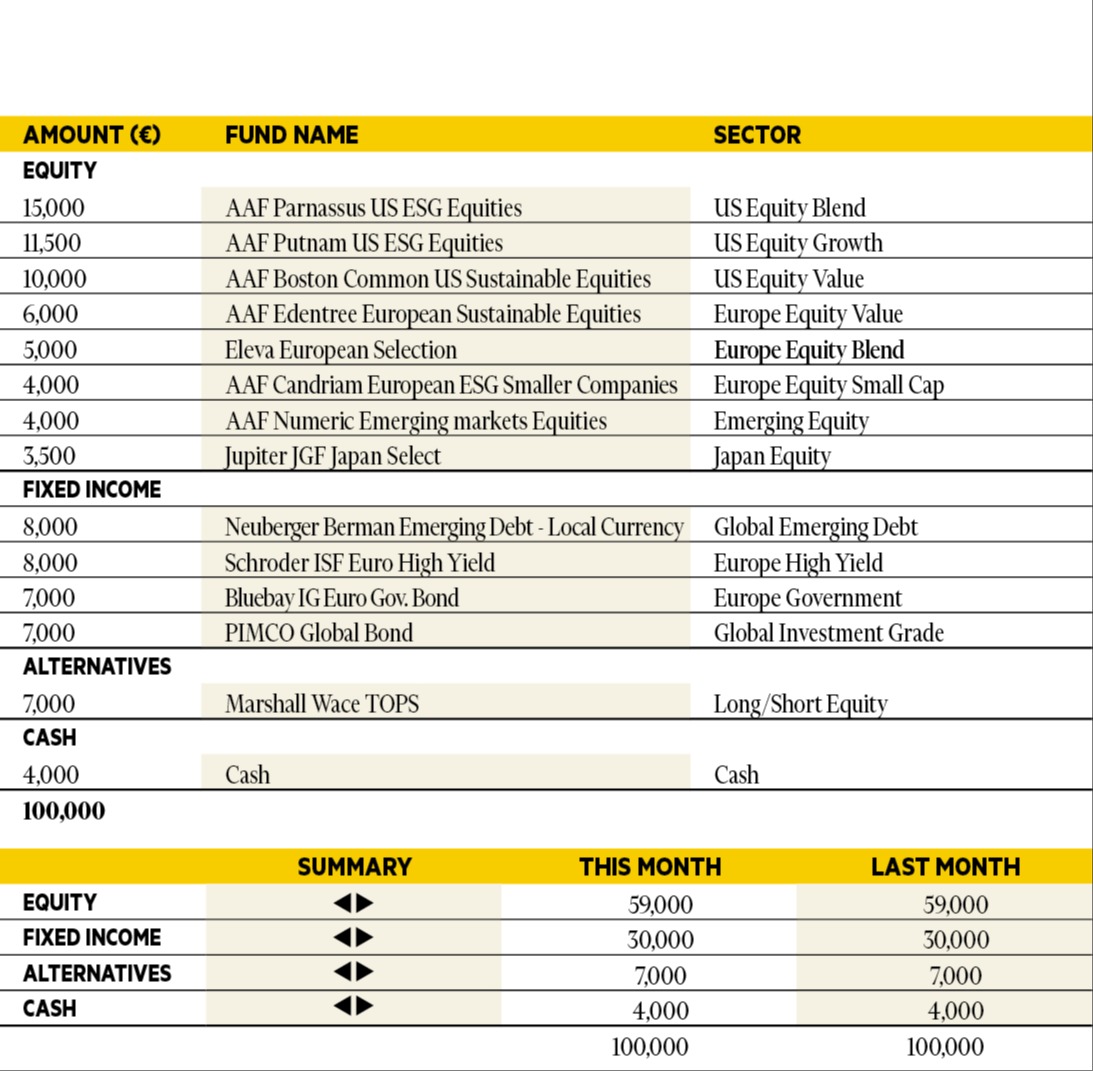

“Global activity and US consumption remain solid. The labour market is slowing but seems to be holding up well at this stage. The recovery in industrial activity, particularly following the US tariff shock, is slow. In the US, services and wealthier households are driving activity, while lower-income households and the industrial sector remain under pressure. The combination of a slightly more accommodating US monetary policy and stimulating economic policies could sustain activity. Sectoral disparities are still significant, with sectors linked to artificial intelligence continuing to be the main drivers. Against this backdrop, the balanced asset allocation is unchanged, with an overall stable preference for equities and emerging markets.”

Luca Dal Mas

Senior fund analyst, Aviva Investors.

Based in: London, UK

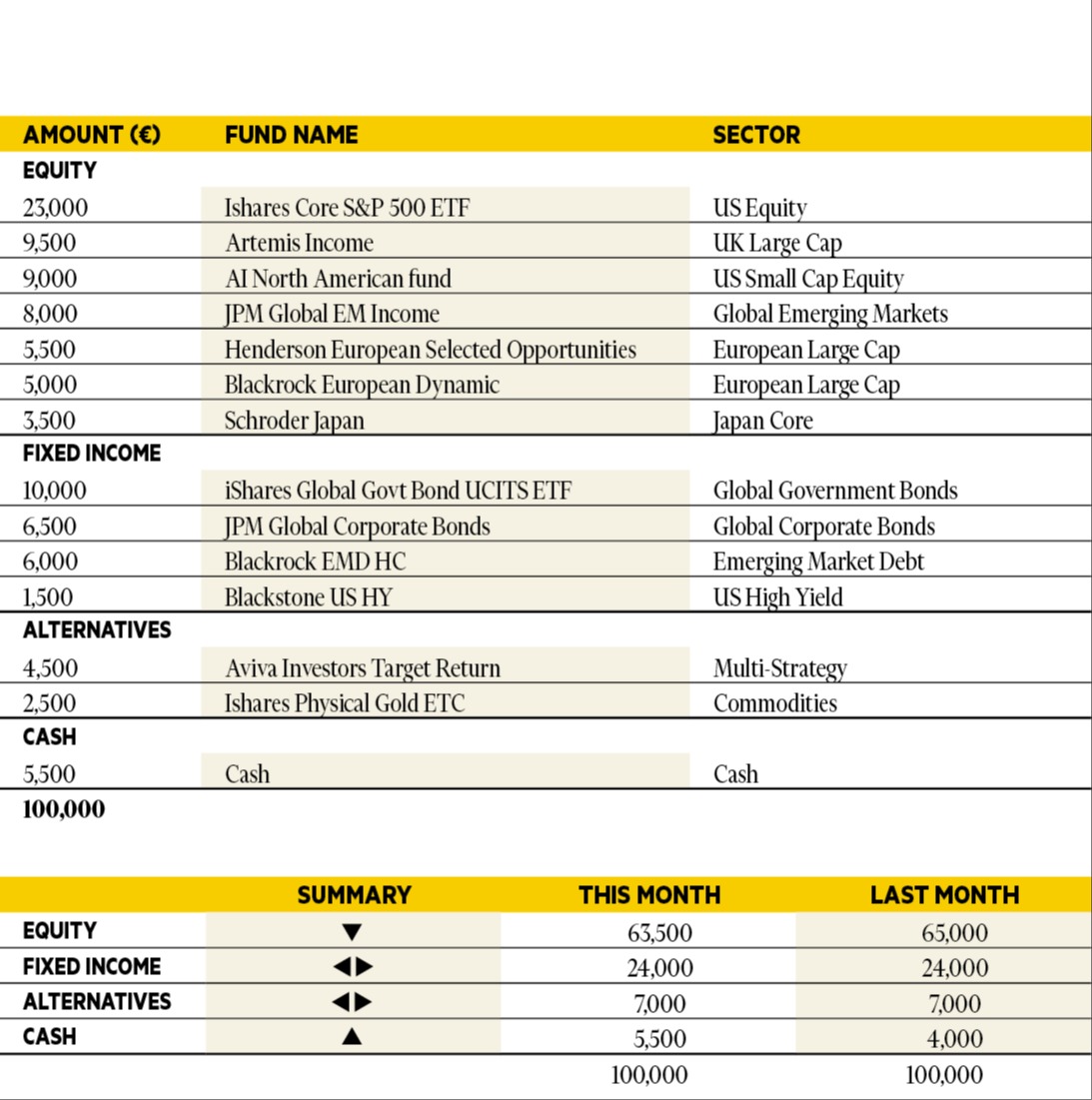

“During the month global markets had mixed performance, with developed economies showing resilience after earlier weakness while emerging markets faced headwinds. US equities remain near record highs despite November volatility, supported by solid corporate earnings and strong survey data, whereas the UK lags amid weak services activity and slowing inflation. In Europe, growth surprised to the upside, reducing hopes for near-term ECB cuts, while Japan benefits from fiscal stimulus. Bond markets offered little protection: US and European yields rose alongside equities, steepening curves, while UK gilts underperformed ahead of the budget. Credit spreads widened modestly, reflecting caution amid high issuance. In portfolios, we continue to actively manage our equity exposure, with a focus towards Europe and US equities.”

Jorge Velasco

Director of Investment Strategy, CaixaBank Private Banking.

Based in: Madrid, Spain

“The most important element of asset allocation is recalibrating the weight of financial assets in the US. Business and economic data reinforce our view that we should maintain an underweight position in that country — both in fixed income and equities. Above all, we should avoid exposure to the dollar as much as possible. When it comes to taking risks, we continue to believe that caution and tactical management (even hyper-tactical management) are the right strategies.”

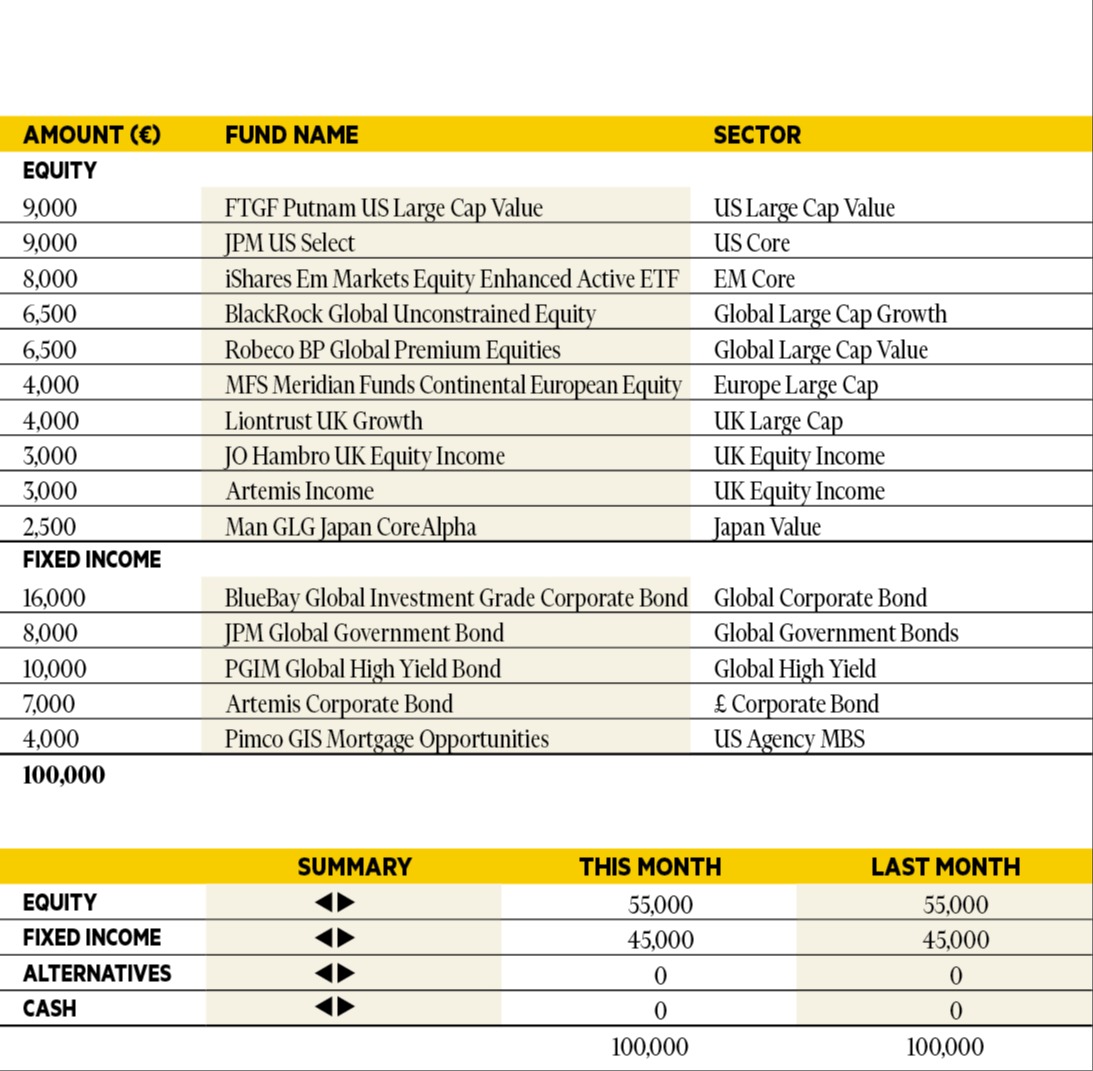

Adam Norris

Portfolio Manager, Columbia Threadneedle Investments.

Based in: London, UK

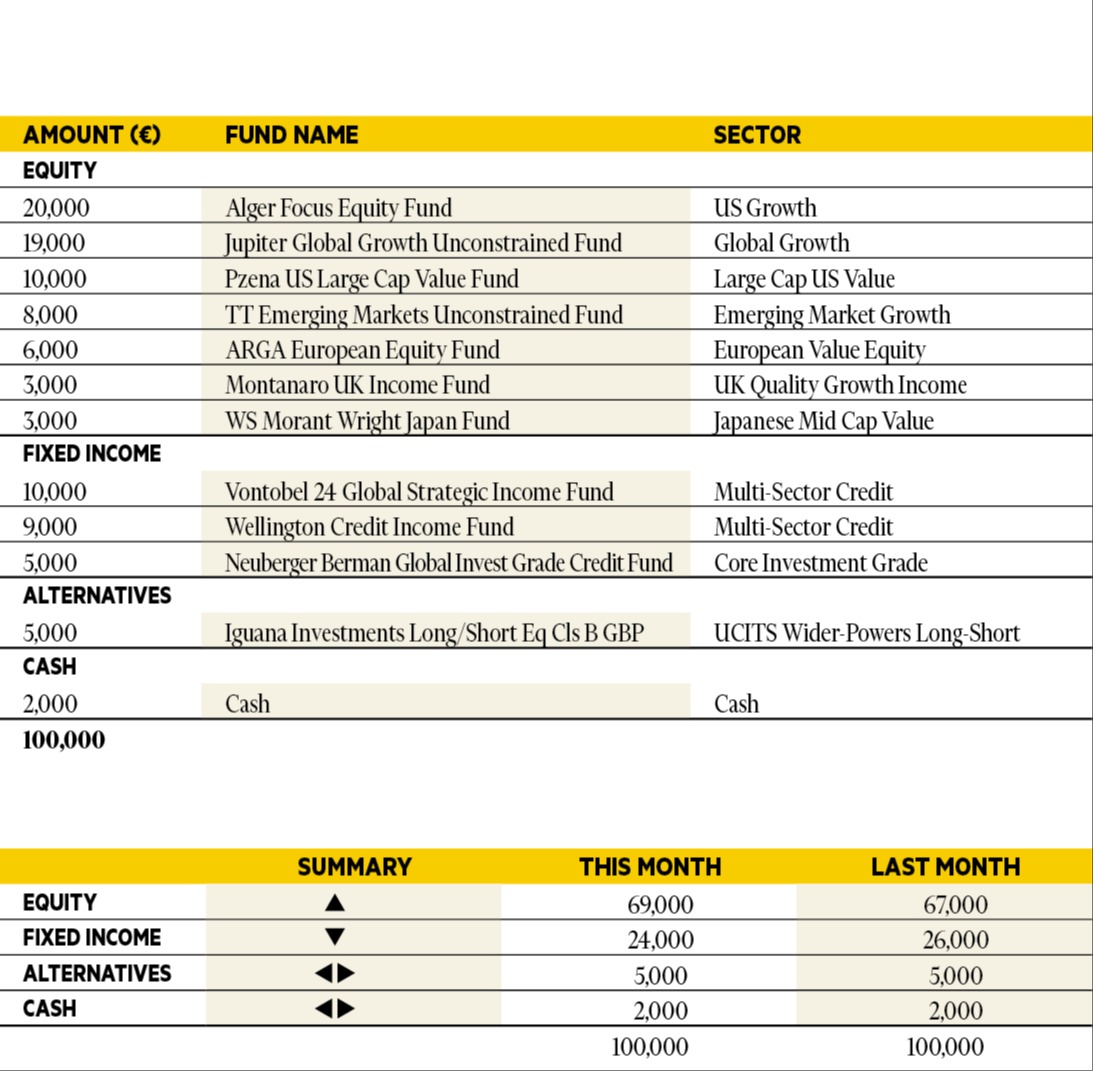

“After a strong run in performance, technology-focused companies pulled back in November, underperforming wider global markets. Credit markets continued to perform strongly, with credit spreads now trading at some over the most expensive valuations in the past 20 years. We used the pullback in US growth equities to add to our position in Alger Focus Equity Fund in our model, trimming investment grade credit. Overall, we remain constructive on risk assets, with a preference for US and emerging market equities.”

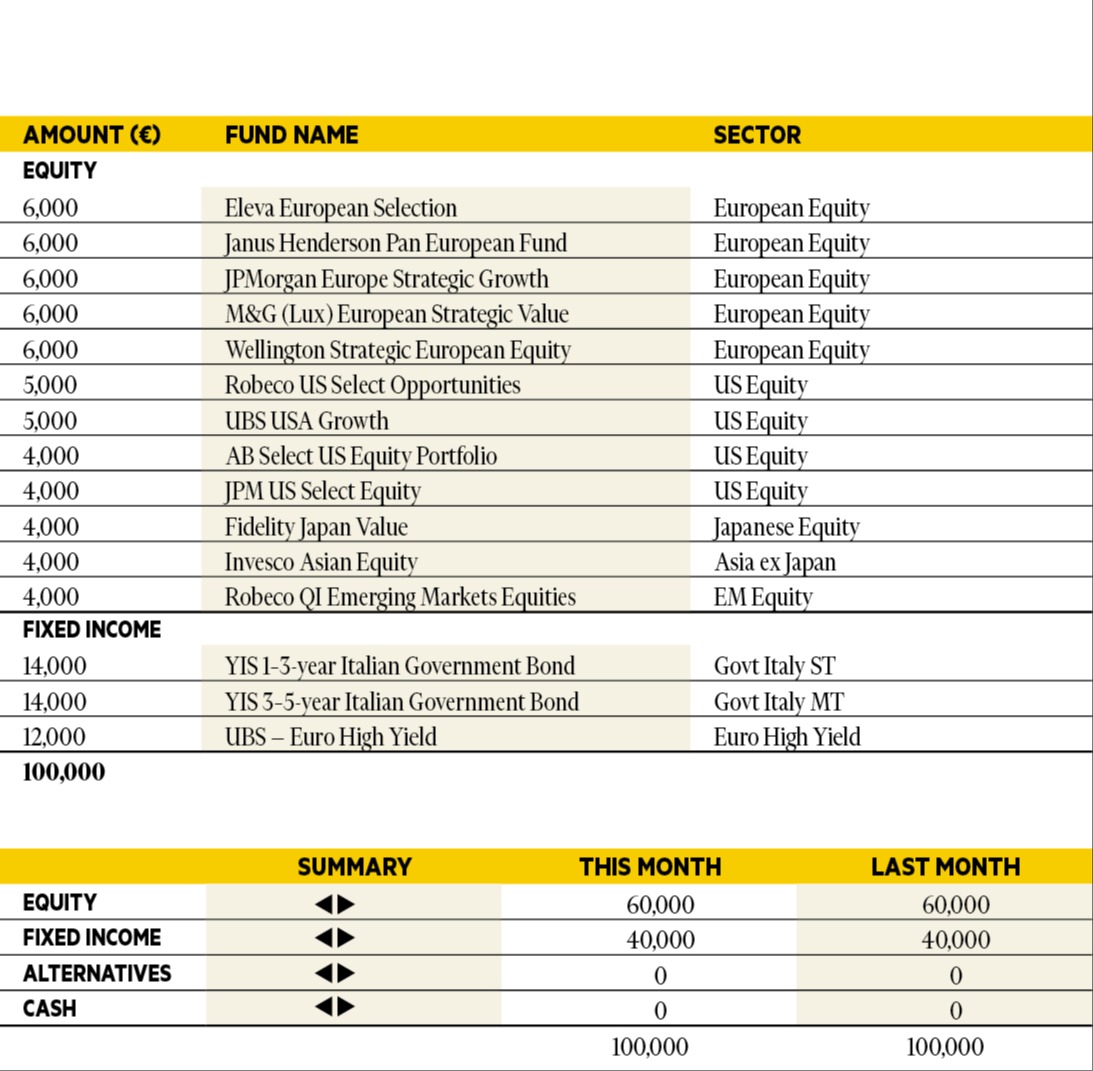

Silvia Tenconi

Multimanager Investments & Unit Linked, Eurizon Capital SGR.

Based in: Milan, Italy

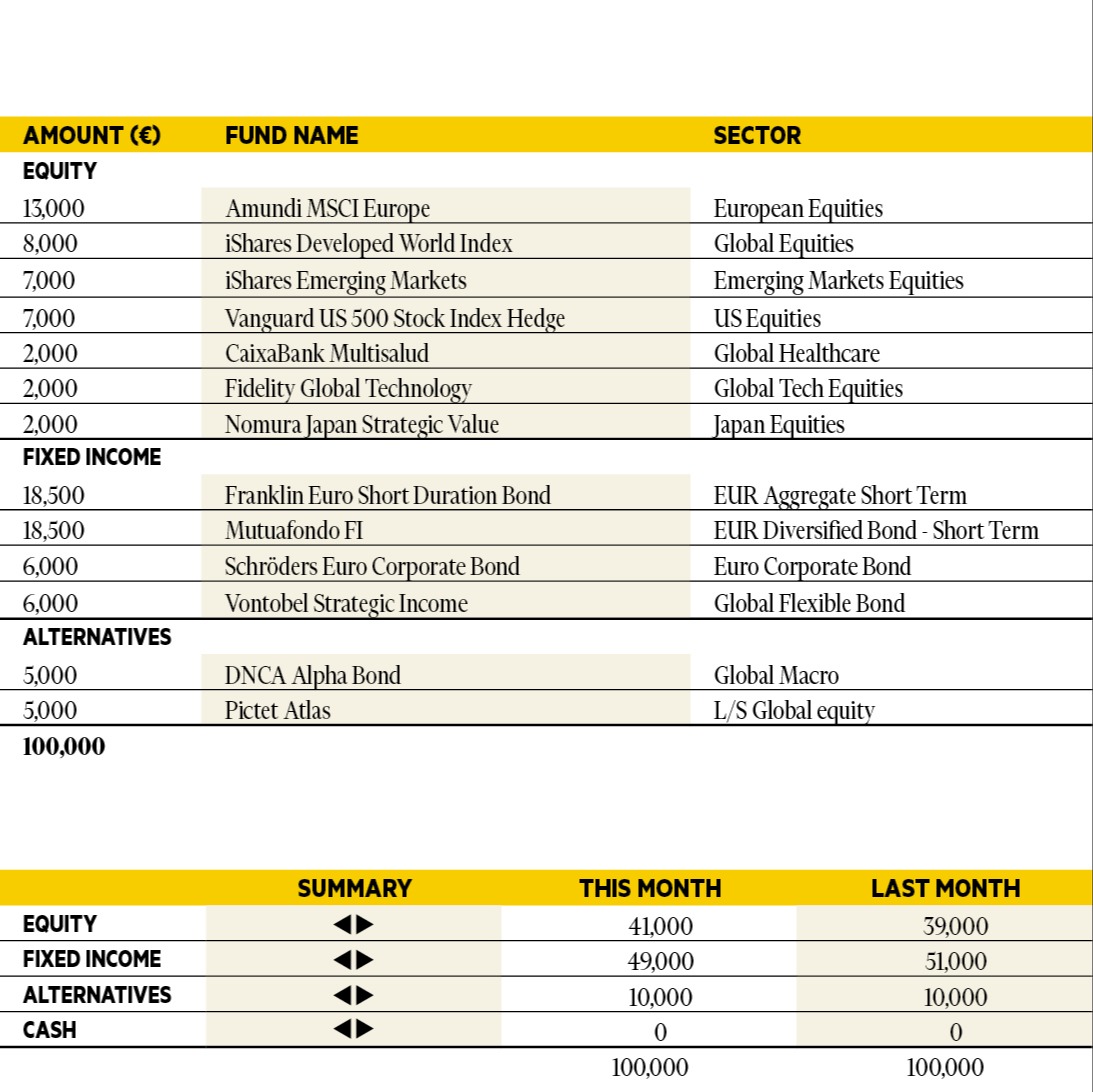

“In November the performance of the portfolio was flat. A bit of pull-back on the emerging and Asian equity funds, and on US growth as well, was compensated by the good results of the European equity funds. The US earning season was better than expected, and the Fed is closer to cutting interest rates, albeit with some reluctance. European credit has a positive month once again, as our Italian govies funds. We keep our allocation unchanged, still favoring Italian govies, Euro high yield, a globally diversified equity exposure and some US dollar.”

Richard Troue

Fund Manager, Hargreaves Lansdown Fund Managers.

Based in: Bristol, UK

“It’s the time of year when my inbox fills with predictions for the year ahead. The only prediction I’ll make is most will be wrong. I try not to obsess over them or join in with my own. They’re useful to the extent they highlight political, economic, and financial risks that could shape 2026. They also highlight less obvious scenarios that could be damaging should they materialise. Most importantly they serve as a reminder to ensure you’re adequately diversified. In this respect I’m happy. One area I’m glad to be invested in is quality shares, via the likes of Liontrust and MSF. They’ve struggled in a market fuelled by AI excitement, but I don’t think they should be written off. At some point they’ll return to favour but given my comments above I’ll refrain from making that an official prediction for 2026.”

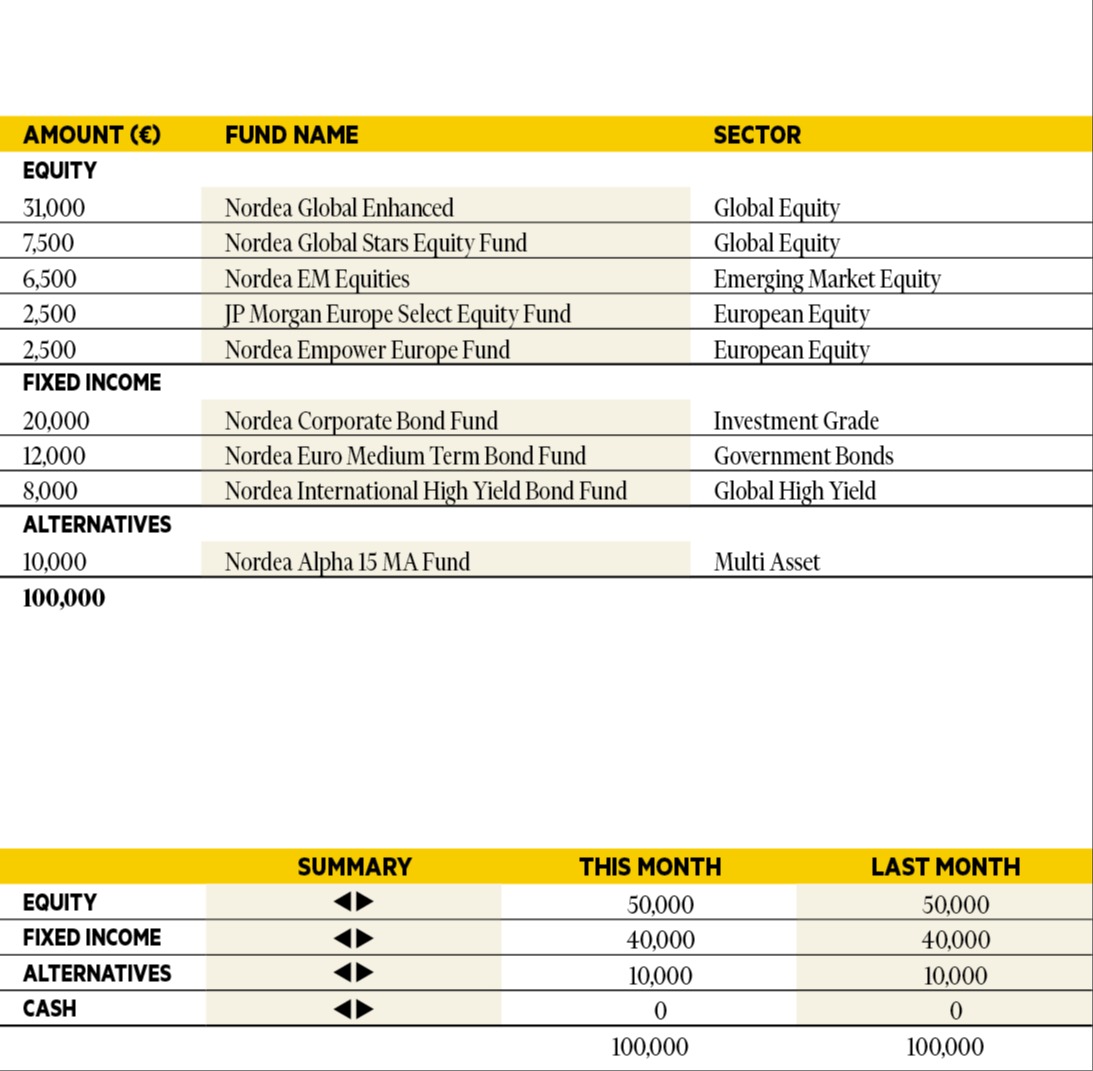

Antti Saari

Chief Investment Strategist, Nordea investments.

Based in: Copenhagen, Denmark

“Markets showed elevated volatility in November, driven by renewed investor skepticism toward major tech names. Ultimately, the downturn proved modest. Despite the turmoil, the month saw several signs of improvement: a strong conclusion to the earnings season, the resolution of the US government shutdown, and renewed hopes for peace in Ukraine. With sentiment now more balanced and fundamentals trending positively, we maintain our overweight position in equities heading into 2026. If anything, we take investor caution towards AI investments as a positive, as such caution reduces the likelihood that excessive exuberance takes hold. At the same time, we also believe that similar episodes are likely in 2026 and investors should be prepared for this. We continue to recommend an overweight for European equities, as we expect the region to benefit from a cyclical recovery, lower rates, and investments in defense and infrastructure.”

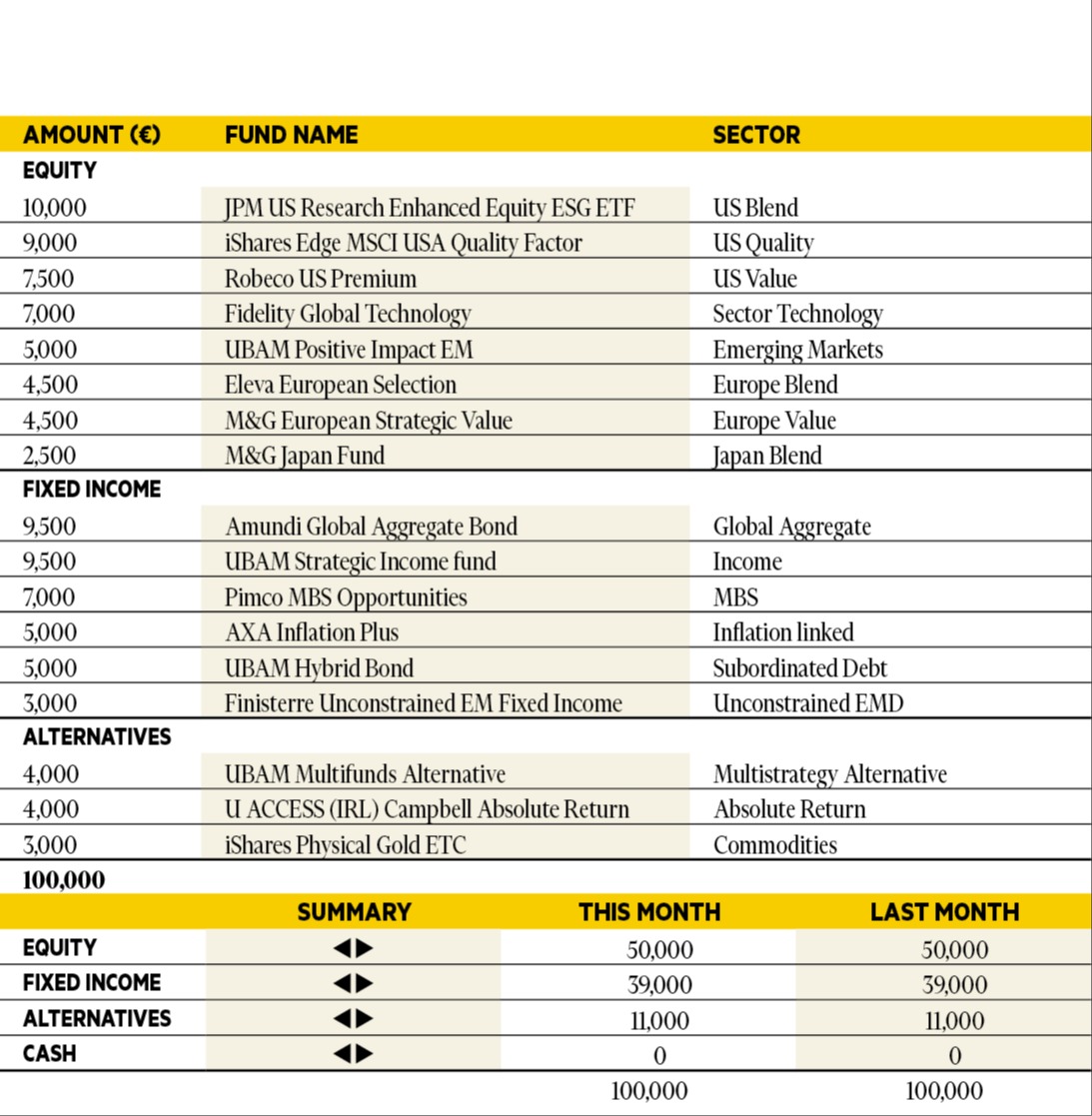

Didier Chan-Voc-Chun

Head of Multi-Management and Fund Research at Union Bancaire Privée (UBP).

Based in: Geneva, Switzerland

“At the start of the month, equity markets were weighed down by concerns about the potential overvaluation of AI companies, but optimism returned with the prospect of a Fed rate cut by year-end. Fixed income markets faced uncertainty due to limited US data and questions about the Fed’s policy direction, while concerns over tariffs and fiscal expansion added to inflation risks. By late November, expectations shifted towards a potential Fed rate cut on 10 December. The third-quarter earnings season wrapped up in November, confirming a strong earnings trend, with technology-related companies delivering particularly impressive results. We continue to maintain our core conviction on US equities, bolstered by favourable economic conditions, resilient household spending, anticipated monetary easing, and robust earnings growth, and we also favour high-yielding segments within fixed income exposures.”